The current AI boom is often, and incorrectly, likened to the dot-com bubble. While both periods share characteristics such as transformative technology, rapid market growth, and investor enthusiasm, a deeper analysis reveals significant structural and financial differences.

The AI boom is marked by a highly concentrated market dominated by profitable established companies, substantial internal capital investment in a specialized and limited supply chain, demonstrable integration into businesses, and proactive government involvement. This creates a distinct risk and opportunity landscape, considerably different from the speculative, fragmented, and unprofitable startup-driven market of the late 1990s. These two cycles are not comparable, and understanding these distinctions is vital for informed strategic decision-making.

Market Concentration vs. Market Fragmentation

Dot-Com Era: The dot-com era was characterized by an explosion of startups driven by a decentralized, speculative 'land grab'. This period saw a frenzy of Initial Public Offerings (IPOs) from nascent, often pre-revenue startups, with 457 IPOs in 1999 alone, contributing to a 400% surge in the Nasdaq between 1995 and March 2000. Startups were the primary disruptors.

AI Boom: In contrast, the current AI boom is an oligopolistic race dominated by a handful of mega-cap technology companies—the so-called 'Magnificent Seven'. These companies are simultaneously the primary researchers, developers, funders, and customers of AI technology. The five largest stocks in the S&P 500 now account for 25% of the index's market cap, a notable increase from 18% in the early 2000s.

These incumbents are projected to invest $400 billion on AI infrastructure in 2025 alone, a figure that dwarfs the entire venture capital market. The IPO market is largely dormant, with capital deployed through massive private rounds or internal R&D/capex budgets. Many AI startups function as ecosystem players or satellites orbiting the incumbent giants, often building upon their foundational models. The most common exit for a successful AI startup is an acquisition by an incumbent, rather than an IPO.

Key Differences: The AI market exhibits greater stability due to the financial strength of these incumbent companies. A potential crash would signify a strategic failure within the world's largest and most profitable corporations, rather than a cascade of failures among small, unprofitable startups.

Eyeballs vs. Earnings

Dot-Com Era: The dot-com bubble saw profitability dismissed, with “eyeballs” and “pageviews” prioritized over earnings. Few tech companies were profitable at IPO, pushing the Nasdaq P/E to 200. Failures like Webvan exemplify this era of flawed business models and operational issues.

AI Boom: In contrast, the current AI boom is anchored by some of the most profitable and cash-rich companies in history, such as Apple (which executed $77 billion in buybacks in 2023) and Microsoft (where AI-related revenue accounts for 54% of total revenue). While many AI startups are not yet profitable, the standards for investment have become far more rigorous. Key metrics now include Annual Recurring Revenue (ARR) and Net Revenue Retention (NRR), with compute-adjusted gross margins being particularly crucial for AI companies.

Key Differences: Despite the massive capital expenditure in AI (the top four tech giants are projected to spend approximately $350 billion on AI in 2025), direct AI revenues are lagging far behind. OpenAI, for example, reportedly projects $12.7 billion in revenue against $14 billion in losses. An MIT study further highlights this paradox, finding that 95% of enterprise generative AI projects have failed to yield any measurable gains in profit.

The unprofitability seen during the dot-com era was driven by a flawed business model belief. In contrast, AI's current unprofitability is driven by immense, front-loaded capital investment in R&D and compute infrastructure.

The primary risk in the current AI landscape is not widespread bankruptcies, but rather a disappointment gap. This could occur if tangible, large-scale productivity gains do not materialize, potentially leading to a repricing of major tech companies.

Oversupply vs. Bottleneck

Dot-Com Era: A speculative overbuild of general-purpose telecommunications infrastructure (fiber optic cable, routers, switches) with over $500 billion invested, much of it debt-financed. This led to immense overcapacity—a glut of 'dark fiber' and unused network equipment—when demand collapsed, causing widespread bankruptcies.

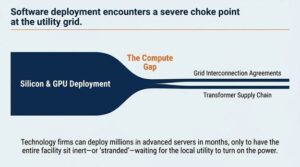

AI Boom: Predicated on a highly specialized, capital-intensive, and critically constrained supply chain for hardware, particularly Graphics Processing Units (GPUs). Total AI infrastructure spending is projected to reach $1 trillion by 2028. This build-out has profound physical-world consequences, particularly in its demand for energy, with tech giants investing in energy production.

Key Differences: Nvidia is the undisputed ‘picks and shovels' provider, commanding an estimated 92% of the market for data center GPUs. Unlike Cisco, Nvidia's dominance is built on a deeply integrated hardware and software ecosystem (CUDA), creating a powerful developer lock-in and a formidable competitive moat.

The global supply of advanced GPUs is severely constrained, with demand far outstripping production, leading to shortages, long lead times, and premium pricing. The supply chain is geopolitically fragile due to dependency on Taiwan Semiconductor.

The fundamental risk has inverted: from a crisis of demand collapse in 2000 to a crisis of supply-side bottleneck in 2025. This, coupled with geopolitical considerations (US CHIPS Act, US-China “digital cold war”), transforms the infrastructure market.

The Bottom Line

The AI boom is not a speculative bubble in the mold of the dot-com era but the next phase of industrial evolution, characterized by technological consolidation and deep economic integration, led by powerful corporations and nation-states.

The market's fate is tied to a very small number of companies. A misstep by Nvidia or Microsoft could have cascading effects. The massive AI capital expenditure relies on unprecedented productivity gains that are proving difficult and slow to realize at scale. A persistent failure to translate AI investment into measurable, bottom-line ROI could lead to a significant market re-rating of tech giants. While the AI boom is not a bubble in the Dot-Com style, there are still significant risks.

The AI, AI Boom vs. Dot-Com Bust

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.