This week’s highlights:

- The “compute gap” represents a significant friction point between the rapid pace of digital innovation and the slow, complex reality of physical infrastructure.

- While software development moves at the speed of light, physical infrastructure is constrained by lengthy permitting processes and construction delays.

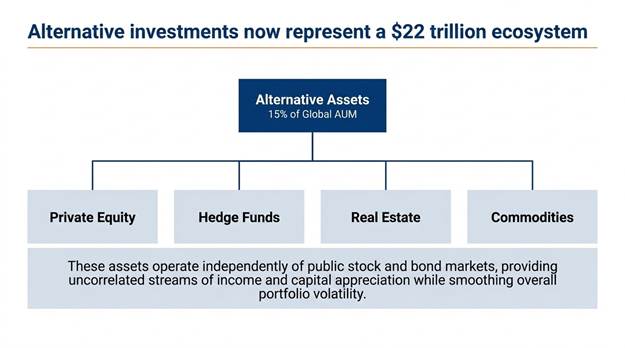

- Halbert Wealth Management views this transition as more than an energy challenge; it is a catalyst for exploring non-traditional, risk-aware investment strategies.

- These strategies aim to help investors navigate market volatility by aligning with the structural realities of this new era.

The Speed of Silicon vs. the Pace of Power

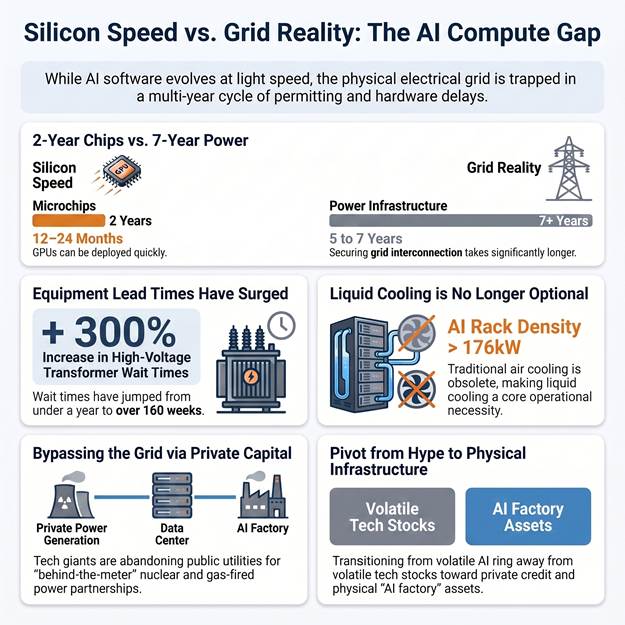

To understand the compute gap, we must contrast two entirely different industrial cycles. On one side is next-generation computing hardware, specifically Graphics Processing Units (GPUs), the advanced microchips designed for parallel processing. These chips can be fabricated, sold, and racked in high-density data halls in a swift 12 to 24 months.

On the other side is the legacy electrical grid, which operates on decadal timelines. Securing a grid interconnection agreement for a new data center now takes a median of five years nationally, stretching past seven years in congested regions like the Mid-Atlantic’s PJM Interconnection.

Furthermore, custom substation equipment like high-voltage transformers faces lead times of over 160 weeks in 2026, compared to less than a year historically. This maturity mismatch means a technology firm can deploy millions in advanced servers in months, only to have the entire facility sit inert, or “stranded”, for years waiting for the local utility to turn on the power.

The Rising Thermal Storm inside the Rack

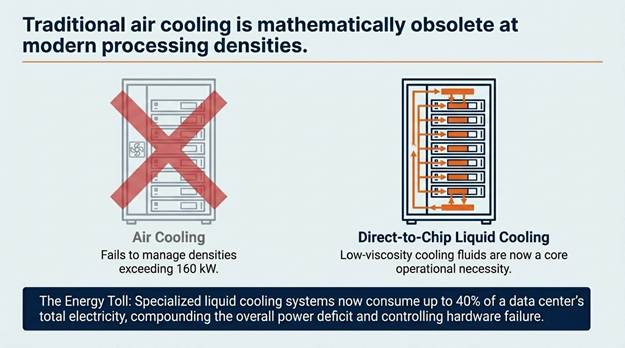

This maturity gap is further compounded by the physics of AI itself. Training frontier AI models requires thousands of GPUs running continuously, causing physical rack power densities to surge from 162 kilowatts (kW) to over 176 kW per square foot, excluding thermal cooling.

Traditional air cooling is simply obsolete at these high densities. Operators are forced to shift to specialized, direct-to-chip liquid cooling and low-viscosity cooling fluids. Because cooling systems consume up to 40% of a data center’s total electricity, these liquid cooling retrofits are no longer a luxury, they are a core operational necessity to prevent hardware failure and control energy waste.

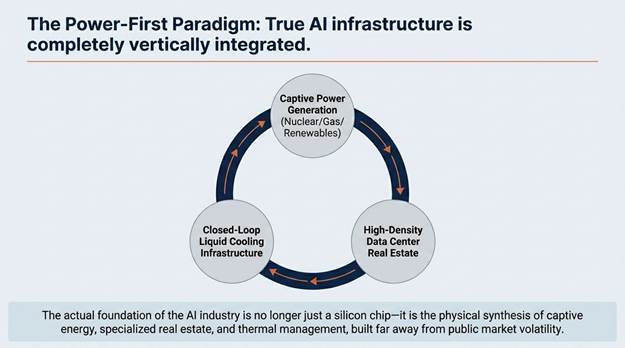

Private Capital’s Captive Workarounds

Faced with an inelastic grid, major tech hyperscalers are no longer waiting on public utilities. Instead, they are partnering with alternative asset managers to bypass the public grid entirely through “behind-the-meter” captive power generation.

Institutional managers are reshaping deployment playbooks around a “power-first” approach. For instance, Blackstone formed a joint venture with PPL Corporation to build gas-fired plants over major shale basins, feeding QTS data centers under long-term Energy Services Agreements. Brookfield integrated its 45-GW renewable portfolio with its subsidiary, Radiant, directly leasing GPUs to tech firms as a vertically integrated “AI factory”.

Furthermore, the nuclear PPA market is experiencing vertical growth, projected to expand from $6.2 billion in 2025 to $47.8 billion by 2034. Google signed a 500-MW agreement with Kairos Power for molten-salt-cooled reactors, while Meta partnered with TerraPower and Oklo, utilizing upfront prepayments to fund site development.

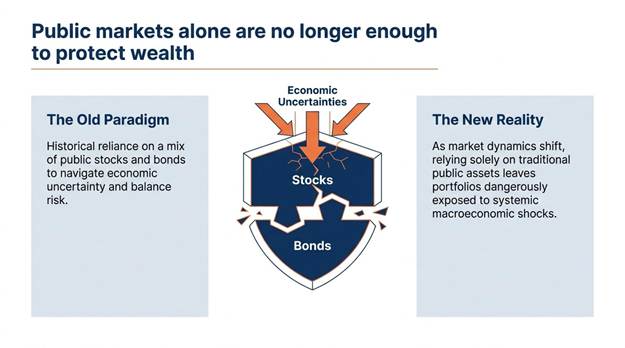

At Halbert Wealth Management, we believe these structural shifts highlight the limitations of traditional “buy-and-hold” public equity strategies.

In a world constrained by physical bottlenecks, a risk-aware, absolute-return philosophy that seeks non-correlated, alternative assets can be a powerful tool for portfolio diversification, providing an educational reminder of how real-world constraints shape modern returns.

What You’re Missing

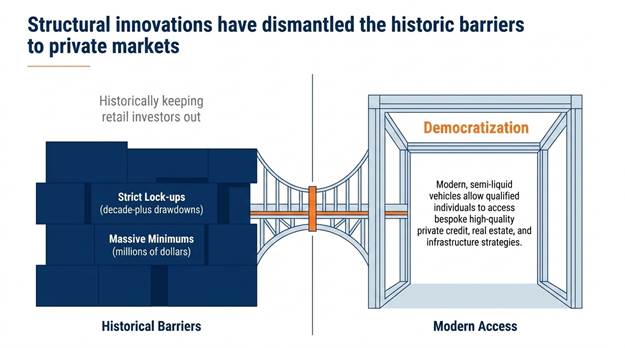

While retail portfolios remain exposed to the volatility of over-hyped tech stocks, institutional investors are quietly moving downstream into the physical stack. What you’re missing are bespoke, institutional-style private offerings that target the physical backbone of this energy transition. By looking beyond public markets to non-correlated alternative assets, such as customized infrastructure portfolios, private credit, or specialized evergreen funds, investors have the potential to align with the structural forces driving grid expansion without daily public market volatility.

Historically, some private-market investments have offered the potential for additional returns associated with reduced liquidity, although such outcomes are not guaranteed.

Want to see where your portfolio might have a power gap?

Schedule a short, no-obligation consultation with our team to discuss how custom-designed alternative investments might fit your personal wealth goals.

Infographic Summary

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.