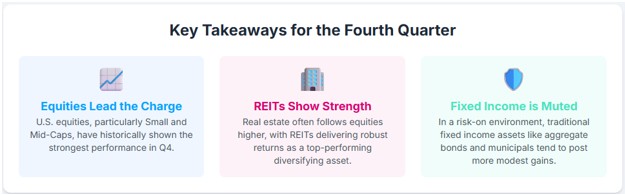

The fourth quarter (Q4) consistently demonstrates strong performance in U.S. equities, outperforming all other quarters. Fixed income assets tend to lag in this period while diversifying and non-standard assets can outperform.

Key Trends in Q4 Equity Performance:

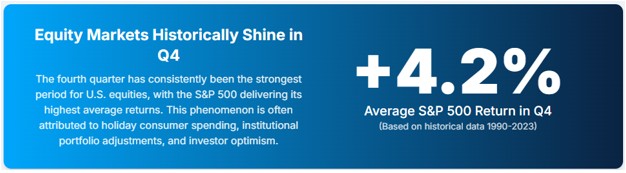

- Overall Equity Outperformance: The average Q4 return for all equity categories is the highest of the year. The U.S. Total Stock Market (VTI) historically shows an average Q4 return of 2.92%. The S&P 500 (SPY) shows an average return of 4.2% in Q4.

- Small-Cap Leadership: Small-capitalization stocks consistently outperform large-cap stocks. The Russell 2000 Index (small-cap) generally yields higher Q4 returns than the Russell 1000 Index (large-cap). Notably:

- Small-Cap Growth (Russell 2000 Growth) leads with an average Q4 return of 7.60%.

- Small-Cap Value (Russell 2000 Value) ranks third at 6.51%.

- Growth Style Dominance: Growth stocks consistently outperform Value stocks across all market capitalizations (large, mid, and small) during Q4.

- Large-Cap Growth (Russell 1000 Growth) ranks second at 6.51%.

- Mid-Cap Growth (Russell Midcap Growth) ranks fifth at 4.70%.

- Sector Leaders: Cyclical sectors, particularly Consumer Discretionary (COND) and Information Technology (INFT), are significant drivers of Q4 equity rallies. Their strong full-year performance often stems from robust performance in the second half, especially in Q4, typically preceded by positive fundamental momentum and upward earnings estimate revisions.

Drivers of Equity Q4 Outperformance

The “Fourth-Quarter Effect” in equities is driven by several key factors:

- Reversal of Tax-Loss Harvesting: The selling pressure on underperforming stocks, particularly small-caps, to realize capital losses diminishes late in the year. This allows their prices to rebound sharply.

- Institutional Window-Dressing: To enhance year-end portfolio appearance, portfolio managers may sell underperforming assets and instead invest in higher-beta or leading stocks, often focusing on small-cap growth.

- Increased Investor Risk Appetite: The fourth quarter is characterized by optimism, holiday spending, and the anticipation of a new year, fostering a “risk-on” sentiment. Investors become more inclined to allocate capital to higher-growth, higher-risk market segments, a category where small-cap stocks are common.

- Positive Earnings Revisions: Analysts typically revise upward their earnings per share (EPS) estimates for growth-oriented sectors like Information Technology and Communication Services as Q4 approaches, which in turn fuels price momentum.

Conditional Performance of Fixed Income and Rate-Sensitive Assets

Unlike equities, the performance of fixed income in Q4 is highly conditional and influenced by macroeconomic factors rather than consistent seasonal patterns.

Core Fixed Income

- Does not show a reliable positive or negative trend in Q4.

- Performance is highly variable, often acting as a counterbalance to risk assets.

- Average Q4 return is 0.46%, the lowest positive return among the analyzed assets.

- Performance is dependent on:

- “Risk-On” environments (bonds typically decline).

- “Flight-to-Quality” environments (bonds tend to rise).

- “Policy-Driven Environments” (e.g., anticipation of rate cuts, as seen with the +6.75% return in Q4 2023).

Municipal Bonds

- Exhibit unique seasonal demand in Q4.

- Driven by tax-loss harvesting and year-end financial planning by high-net-worth individuals seeking tax-exempt income.

- This can lead to a seasonal surge in demand, providing a supportive technical backdrop for the asset class.

Inflation-Linked Securities

- Q4 performance is contingent on the evolving outlook for inflation and real yields.

- Average Q4 return is 0.53%.

- A strong economy presents a dual effect: boosting inflation expectations (positive) but also raising real yields (negative for prices).

Leveraged Bank Loans

- These are floating-rate instruments.

- Q4 returns are typically stable and positive, primarily reflecting the collection of three months of interest payments.

- Returns are driven by high coupon income and are largely delinked from the volatility of the underlying interest rate markets.

- Trailing 3-month return was +2.12% (as of early September 2025).

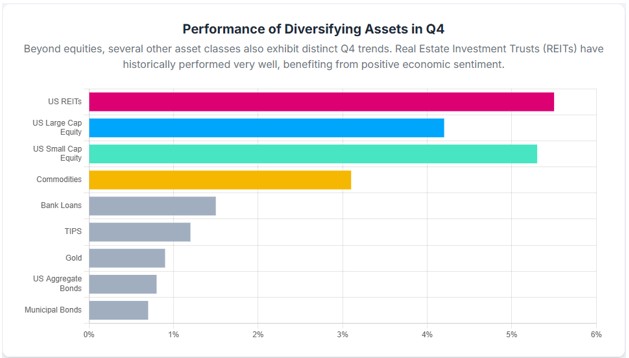

Diversifiers and Real Assets: Divergent Paths

Commodities: These are generally pro-cyclical, meaning they tend to perform well when global economic growth is robust or expected to strengthen. A strong “risk-on” rally in equities during Q4, especially if driven by optimism about future economic growth, typically correlates with increased demand for energy and industrial inputs.

Gold: Primarily considered a safe-haven asset, gold exhibits an inverse correlation with the U.S. dollar and real interest rates. During strong “risk-on” Q4 equity rallies, the demand for safe havens usually diminishes, creating a headwind for gold prices. Gold's strongest periods often coincide with economic uncertainty or crisis, like now.

Real Estate Investment Trusts (REITs): As a “hybrid asset,” REITs are sensitive to both equity market sentiment and interest rates. Being publicly traded equities, REITs benefit from the same “risk-on” appetite that frequently drives the broader stock market higher in Q4. However, as high-dividend-paying instruments, they directly compete with fixed income, making them highly sensitive to changes in Treasury yields. The significant -8.2% decline in the FTSE All Equity REIT Index in Q4 2024 illustrates their sensitivity to rising rates. An ideal Q4 environment for REITs would feature steady economic growth combined with stable or falling interest rates.

The Bottom Line

The effect is not uniform; small-capitalization stocks and growth-oriented equities show the most significant Q4 returns. In contrast, fixed income and other rate-sensitive assets demonstrate more conditional Q4 performance, largely tied to macroeconomic conditions and monetary policy expectations rather than consistent seasonal patterns. Similarly, diversifying assets such as commodities and gold exhibit varied trends based on economic sentiment.

The Q4 AI Effect

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.