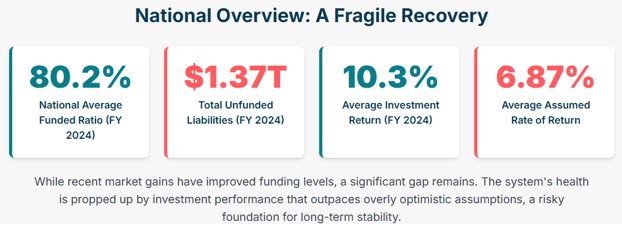

Are underfunded state pensions the next crisis in the making? Maybe. The financial health of U.S. state pension systems has improved recently, but this progress is built on a fragile foundation, exposing deep structural risks that threaten long-term sustainability. The national average funded ratio rose from 75.5% in FY 2023 to an estimated 80.2% in FY 2024, with total unfunded liabilities decreasing from $1.64 trillion to $1.37 trillion. Projections for FY 2025 suggest a modest continued improvement, with the aggregate funded ratio between 77.7% and 82.0% and unfunded liabilities around $1.35 trillion. Despite these gains, the average funded ratio has remained below the 90% “fiscally resilient” threshold for 17 consecutive years.

Factors Responsible for Shortfall Reduction

- Strong Investment Returns: A significant factor in recent improvements has been the exceptional performance of financial markets. In FY 2024, plans saw an average investment return of 10.3%, considerably exceeding the 6.87% average assumed rate of return (ARR). While this boosted plan assets, projections for FY 2025 are a more modest 5.41%, which falls short of the ARR, highlighting the ongoing need for strong market performance to bridge funding gaps.

- Increased Employer Contributions: Employer pension contributions reached a record 31.65% of payroll in 2025, with over two-thirds used to pay down unfunded liabilities. This diverts over 5% of national direct general expenditures to pension debt, limiting funds for public services. States consistently paid 100% of actuarily determined contributions (ADCs) from 2022-2024, showing improved fiscal discipline.

Persistent Structural Challenges

- Overly Optimistic Actuarial Assumptions: The ARR has remained at 6.87% for four years. Most independent analyses suggest this is too optimistic for the current economic climate, with a more prudent range being 5.5% to 6.5%. This inflated ARR systematically understates the true present value of a plan's liabilities and the required contributions.

- Substantial Existing Debt: Aggregate unfunded liabilities have consistently exceeded $1 trillion since the 2008 Financial Crisis, indicating a chronic, structural problem. This long-term debt accrues interest, significantly contributing to the growth of liabilities.

Examples of Funding By State

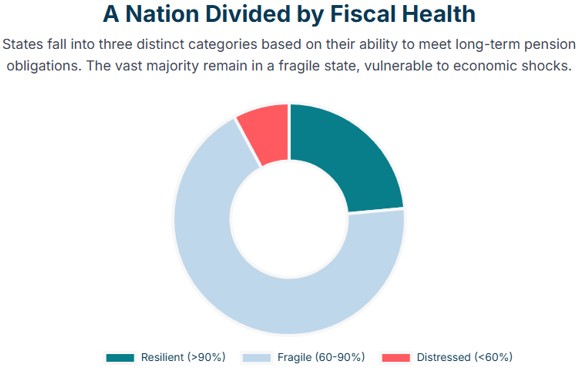

National averages can be misleading when examining state pension funding, as there's a clear divide into distinct tiers of fiscal solvency. States are categorized by their FY 2024 aggregate funded ratio:

- Resilient (90% or higher): Approximately 21% of state pension plans are considered well-funded and have a high probability of meeting their long-term obligations. Examples include the District of Columbia (112.5%), Nebraska (108.5%), Tennessee (107.9%), Utah (104.2%), Washington (102.5%), Wisconsin (102.1%), West Virginia (100.4%), South Dakota (100.0%), Minnesota (93.2%), New York (92.8%), Iowa (91.6%), and Virginia (90.8%).

- Fragile (60% to 90%): This category represents the majority of U.S. pension plans. These systems are vulnerable to economic downturns, investment underperformance, or insufficient contributions. Examples include North Carolina (89.1%), Florida (83.8%), Texas (82.4%), Ohio (81.2%), Michigan (80.9%), California (80.7%), and Pennsylvania (70.3%).

- Distressed (below 60%): These systems face severe structural deficits that pose a significant and ongoing risk to their fiscal stability and ability to meet future benefit payments. Examples include Mississippi (57.0%), New Jersey (56.6%), Kentucky (54.1%), and Illinois (51.6%).

Case Studies of Stress and Stability

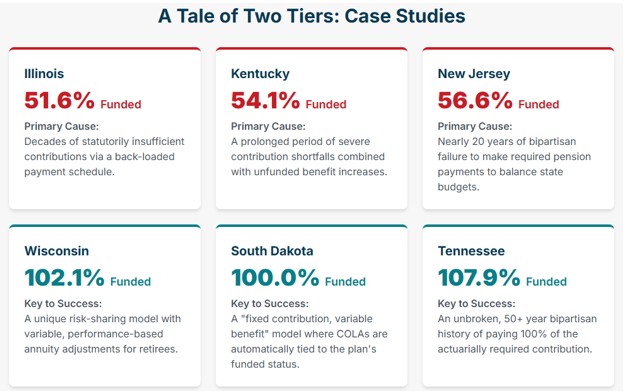

Consider this infographic. It outlines stable vs. unstable pension plan strategy.

State Plans Under Stress

Stress Cases in Underfunding:

- Illinois: Facing the most severe crisis with a 51.6% funded ratio and over $211 billion in unfunded liabilities. Unfunded benefit enhancements, like a 3% automatic compounded Cost of Living Adjustment (COLA), exacerbated the issue. A strict constitutional pension protection clause has made altering benefits for the existing workforce nearly impossible.

- Kentucky: Kentucky's pension plans, 54.1% funded with a $38.5 billion deficit, were fully funded in 2000. Subsequent underfunding by the state legislature, which failed to make full ARC contributions, and unfunded benefit enhancements, led to asset depletion. This forced the plan to sell investments during the Great Recession, incurring permanent losses.

- New Jersey: New Jersey's pension crisis, ranking third-worst funded at 56.6% with $91.1 billion unfunded, stems from nearly two decades of state leaders failing to make required contributions. Reforms like suspended COLAs, causing retirees to lose 35% of their purchasing power. Governance failures and political deal-making also contributed to the problem.

Here are examples of well-funded state pension systems:

- Wisconsin (102.1% funded): The Wisconsin Retirement System (WRS) is lauded for its risk and cost-sharing design between employers and employees. Its shared funding model equally splits contributions to cover benefit costs. Retiree annuity adjustments, or dividends, are tied to investment performance, not guaranteed COLAs, acting as a strong automatic stabilizer.

- South Dakota (100.0% funded): The South Dakota Retirement System (SDRS) uses a fixed contribution, variable benefit model. Member and employer contribution rates are modest (6% each). A variable, performance-based COLA, tied to CPI and a funded ratio affordability test, maintains balance. If the funded status is below 100%, the maximum COLA is reduced to ensure long-term solvency.

- Tennessee (107.9% funded): TCRS's success stems from consistent fiscal discipline, including fully funding its actuarially determined contribution since 1972. In 2014, Tennessee reformed its system, moving new hires to a hybrid plan combining a defined benefit with a state-matched 401(k), sharing market risk and stabilizing costs.

States with well-funded pension systems offer a clear road map for successful pension management. Their success stems from deliberate policy choices and plan designs that enforce fiscal discipline, manage risk, and insulate the systems from political pressures.

The Bottom Line

Is there a looming state pension crisis? Not on a national scale, but potentially by state. It is clear from this basic look that a bifurcation is taking place. Most pensions are fine. But the ones that are teetering, Illinois being the worst, could eventually require extreme action, maybe even a bailout at the federal level.

AI Pensions

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.