Stablecoins vs. SWIFT: Remodeling Global Payments

Stablecoins are shaking up the digital asset world by offering a stable alternative to the wild price swings of cryptocurrencies like Bitcoin. By pegging their value to more stable assets, often fiat currencies like the U.S. dollar, they're finding their way into cross-border payments, traditional finance, and even government experiments with money. This article will dive into the rise of stablecoins, how they measure up against the SWIFT network, and what this all means for the future of how we move money.

Stablecoins: The Digital Dollar Evolved

Stablecoins are a unique form of digital token engineered to maintain a steady value, usually by linking their value to something stable, like the U.S. dollar. This stability is key to making them more practical for everyday use as a medium of exchange and a reliable store of value. Think of them as a bridge connecting the fast-moving crypto space with the familiar reliability of traditional currencies.

The mechanics of how stablecoins achieve this stability are quite interesting, revolving around the concept of a “peg”. The peg is the specific value relationship a stablecoin aims to maintain, such as 1 stablecoin always equaling 1 U.S. dollar. This stability isn't a given; it's actively managed through various mechanisms.

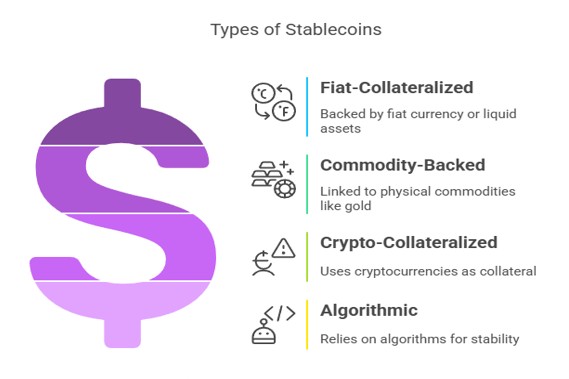

Decoding Stablecoin Types

Stablecoins come in several flavors, each with a distinct approach to maintaining value:

- Fiat-Collateralized Stablecoins: The most common type, these stablecoins are backed by reserves of fiat currency or highly liquid assets like government bonds. Prominent examples include Tether (USDT) and USD Coin (USDC).

- Commodity-Backed Stablecoins: These stablecoins link their value to physical commodities such as gold, offering a way to invest in commodities without direct ownership. PAX Gold (PAXG) is a notable example.

- Crypto-Collateralized Stablecoins: Instead of fiat, these stablecoins use other cryptocurrencies as collateral. Due to the volatility of crypto, they typically employ over-collateralization, meaning they hold more in collateral than the stablecoin's value. MakerDAO's Dai (DAI) is a prime example.

- Algorithmic Stablecoins: These stablecoins rely primarily on algorithms to control their supply and maintain the peg, often with limited or no collateral. This type is considered riskier, highlighted by the collapse of TerraUSD (USTC).

Each type carries its own risk profile. Fiat-backed stablecoins are subject to issuer and reserve risks, crypto-collateralized stablecoins to the volatility of the underlying crypto, and algorithmic stablecoins to the stability of their algorithms and market confidence.

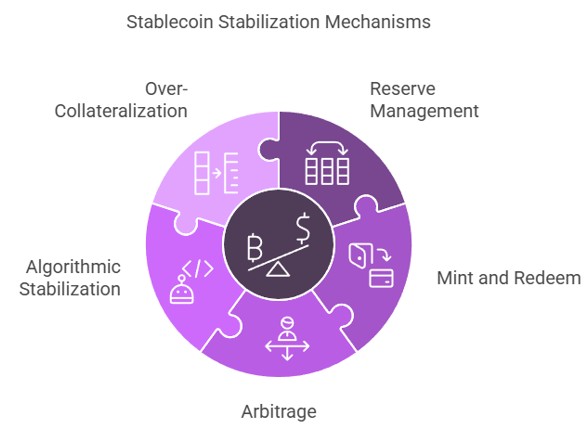

The Stability Playbook

Stablecoins employ several mechanisms to defend their stability:

- Reserve Management: Stablecoin issuers hold reserves equal to the tokens in circulation, backing the issued stablecoins with assets like cash and bonds.

- Mint and Redeem: Issuing companies create (“mint”) and destroy (“redeem”) stablecoins to maintain parity with their reserves, establishing the stablecoin's intrinsic value.

- Arbitrage: Market makers help maintain the peg by engaging in arbitrage, buying or selling stablecoins when their price deviates from $1.

- Algorithmic Stabilization: Algorithmic stablecoins use code to adjust the circulating supply in response to price fluctuations.

- Over-Collateralization: Crypto-backed stablecoins use this method, requiring more collateral than the value of the issued stablecoins, to absorb potential price drops.

It's crucial to acknowledge that stablecoins, despite their name, aren't inherently “stable.” They face risks like losing their peg, runs on the issuer, and vulnerabilities in their underlying mechanisms.

Stablecoins Take Center Stage

The stablecoin market has experienced explosive growth, with transaction volumes reaching impressive levels. While the market is concentrated around a few major issuers like Tether (USDT) and USD Coin (USDC), stablecoins are finding diverse applications.

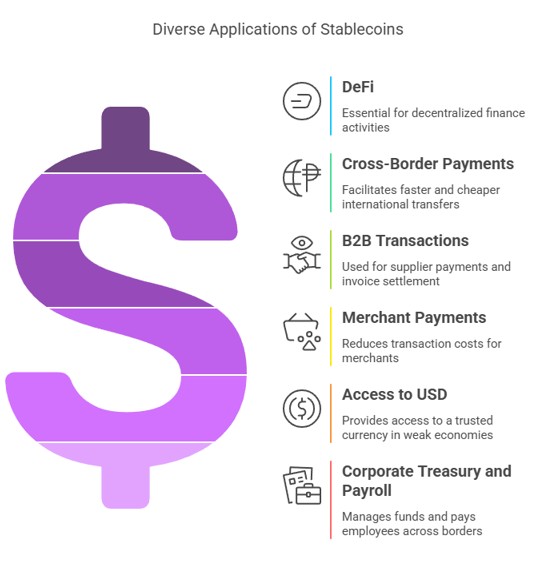

Beyond their initial use in crypto trading, where they offer a stable way to enter and exit volatile positions, stablecoins are now used in:

- DeFi: They're essential for decentralized finance, facilitating trading, lending, borrowing, and yield farming.

- Cross-Border Payments: Stablecoins offer the potential for faster, cheaper, and more accessible international money transfers, bypassing the delays and fees of traditional systems like SWIFT.

- B2B Transactions: Businesses are leveraging stablecoins for supplier payments, invoice settlement, and treasury management.

- Merchant Payments: Stablecoins can lower transaction costs for merchants compared to credit card processing fees.

- Access to USD: In countries with weak currencies or limited access to U.S. dollars, stablecoins provide an alternative way to save and transact in a trusted currency.

- Corporate Treasury and Payroll: Companies use stablecoins for managing funds and paying employees, especially across borders.

Governments are also exploring stablecoin technology through pilot programs, recognizing their potential and cautiously assessing the risks.

Stablecoins and the Strategic Importance of the U.S. Dollar

Stablecoins, by increasing the distribution and liquidity of U.S. dollars in the digital realm, reinforce the dollar's dominance as a global trading and transaction vehicle. This is strategically important for the U.S. because the dollar's strength allows the U.S. government to borrow at low rates and maintain economic influence.

According to crypto expert and venture capitalist David Sacks, “Stablecoins have the potential to ensure American dollar dominance internationally, expanding digital-dollar use as the world’s reserve currency and creating potentially trillions of dollars of demand for U.S. Treasuries.”

Stablecoins vs. SWIFT: A Detailed Comparison

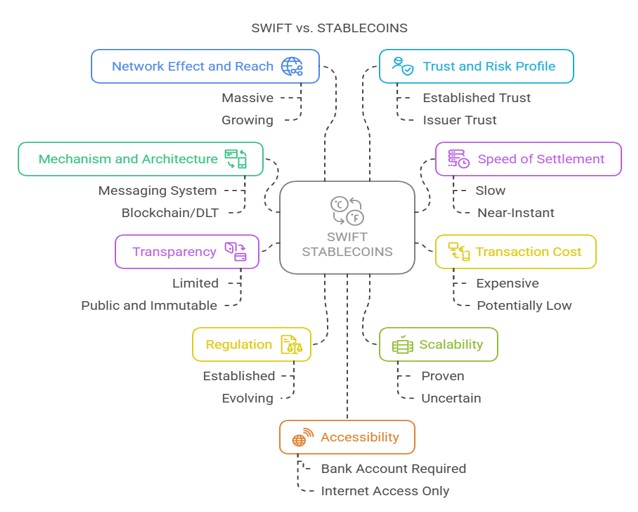

Understanding the Systems

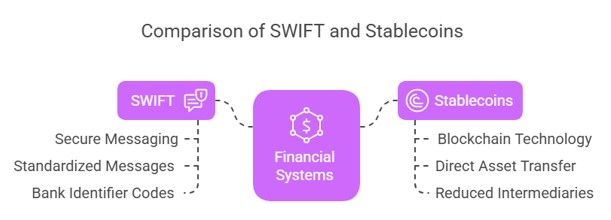

- SWIFT is primarily a secure messaging network. It was created to standardize financial messages between institutions globally, replacing older methods like Telex. SWIFT does not hold funds or transfer assets itself. Instead, it sends payment instructions between banks. The actual money transfer and settlement happen outside the SWIFT network, often through a chain of correspondent banks holding accounts with each other. This system relies on standardized message types and unique Bank Identifier Codes (BICs).

- Stablecoins are a type of cryptocurrency designed to maintain a stable value relative to an external asset, usually a fiat currency like the US dollar. They are built on blockchain or distributed ledger technology (DLT). Unlike SWIFT, which is just messaging, stablecoins can facilitate the direct transfer of the digital asset itself, aiming to reduce or remove the need for multiple intermediaries in the transfer process.

Key Differences

- Mechanism and Architecture: SWIFT facilitates interbank communication through a messaging system that relies on correspondent banking for settlement. In contrast, stablecoins are digital assets leveraging blockchain/DLT, offering the possibility of peer-to-peer or near-peer-to-peer transfers with built-in settlement.

- Speed of Settlement: Stablecoins enable almost immediate settlements, completing transactions within seconds or minutes and operating continuously. In contrast, SWIFT cross-border payments are typically slow, requiring one to five business days due to banking hours and intermediary involvement. Although SWIFT GPI (Global Payments Innovation) seeks to enhance speed, final credit confirmation can still experience delays.

- Transaction Cost: Stablecoins offer the potential for very low transaction fees by disintermediating processes. However, users might encounter costs related to fluctuating blockchain gas fees and charges for converting between stablecoins and traditional currencies. In contrast, SWIFT transactions tend to be costly due to layered fees from various banks and often include unclear and unfavorable foreign exchange rate markups.

- Transparency: Stablecoin transactions offer transparency through their recording on public and unchangeable ledgers, albeit often with pseudonymous identities. In contrast, traditional SWIFT payments historically lacked comprehensive end-to-end tracking, a limitation that SWIFT GPI has addressed by offering improved tracking capabilities.

- Regulation: Stablecoins operate within an evolving, fragmented, and often uncertain global regulatory landscape. SWIFT functions within established, well-defined global financial regulatory frameworks and is deeply integrated into existing legal systems.

- Scalability: While stablecoins are addressing historical scalability issues like network congestion and fees, their ability to manage the immense daily global payment volume handled by SWIFT remains unproven. SWIFT's existing infrastructure demonstrates a strong capacity for processing vast transaction volumes.

- Network Effect and Reach: While stablecoins are expanding their network, especially within the digital asset realm, their reach is considerably smaller than SWIFT's. SWIFT possesses an extensive and well-established global network, linking over 11,000 financial institutions across more than 200 countries, which provides it with significant momentum.

- Trust and Risk Profile: Stablecoins carry risks tied to the reliability of their private issuers, the quality and openness of their reserve assets, and the possibility of sudden withdrawals or technological issues. Algorithmic stablecoins are especially high-risk. In contrast, SWIFT has built substantial trust over decades with regulated financial entities and governments. SWIFT's risks typically involve the security of member banks' systems or political events such as sanctions.

- Accessibility: Stablecoins could improve financial inclusion for individuals lacking bank accounts by only needing internet access and a digital wallet. In contrast, access to SWIFT necessitates an affiliation with a financial institution, typically requiring a bank account.

- Intermediaries: Stablecoins seek to minimize or remove intermediaries in transaction processes. In contrast, SWIFT's structure depends significantly on a network of correspondent banks, which introduces greater complexity, higher costs, and potential for delays.

The Regulatory Landscape and CBDCs

The rise of stablecoins has caught the attention of regulators worldwide. There's a big push for global coordination to ensure fair rules and prevent regulatory arbitrage. However, different jurisdictions are taking different approaches, which can create complexity.

Adding another layer to the mix, central banks are also exploring their own digital currencies, known as CBDCs. These could potentially compete with stablecoins or coexist in the future financial landscape.

The Future of Finance

The future of finance is at a crossroads, with stablecoins, CBDCs, and traditional systems all vying for a role. We could see competition, but more likely, we'll see these different forms of money find their own niches and perhaps even work together.

Ultimately, how this all plays out will depend on things like regulation, technological advancements, user adoption, and even geopolitical factors.

Stablecoins are changing the way we think about money, especially when it comes to sending money across borders. They're not going to replace everything overnight, but they are pushing the financial world to become faster, cheaper, and more accessible.

AI International Monetary Transfers

[Spencer]

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.