What the major investment banks are saying about 2026.

2026’s fundamental economic shift replaces pure efficiency and seamless globalization with a new focus on resilience and security, reshaping core economic inputs through strategic adjustments like:

- Energy redundancy

- Supply chain near-shoring

- Increased defense expenditures

The End of Global Synchronization (The K-Shaped Economy)

The “K-shaped economy” is a concept used to describe a post-expansion period of significant economic divergence, where different sectors or regions recover or perform at different rates that look like a letter ‘K’.

The coordinated global expansion of the past decade is over, replaced by significant economic divergence. Analysts, including Bank of America and J.P. Morgan, describe this fragmentation using the “K-shaped” recovery concept, applied both sectorally and regionally.

- Sectoral Divergence: Capital-intensive industries (e.g., technology, energy infrastructure, and defense) are poised to decouple and outperform. In contrast, interest-rate-sensitive sectors (e.g., traditional real estate and consumer discretionary) are projected to lag.

- Regional Divergence: The trend of “US Exceptionalism” persists. U.S. GDP growth forecasts consistently exceed those of other developed markets, underpinned by energy independence and technological leadership. While Europe is expected to stabilize, it will likely trail, and the growth advantage of emerging markets over developed markets is narrowing.

The Three Pillars Shaping the 2026 Economy

Three structural forces are identified as the key drivers of upcoming economic outcomes:

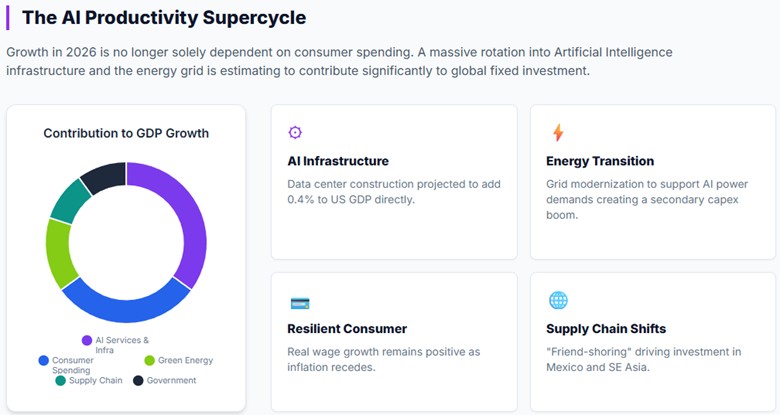

- The AI Supercycle: This cycle is moving from the initial building phase (capital expenditure) to the using phase (productivity gains). The potential arrival of “agentic” AI models achieving human-level performance by spring 2026 is noted by J.P. Morgan as a major catalyst for a productivity boom.

- Fiscal Activism and Industrial Policy: Major governments, particularly the U.S. and Germany, are transitioning from fiscal consolidation to active industrial policy.

- Economic Nationalism: Tariffs are evolving from temporary negotiating tactics into a permanent component of the global system. This trend is expected to increase inflation volatility and necessitate a significant reorganization of global capital flows.

U.S. Economic Outlook

The forecast for the U.S. economy, the key driver of the global outlook, is currently split between two major institutional viewpoints: the Bullish Re-accelerationists and the Cautious Structural Sceptics.

The Bullish Case: Re-acceleration

This optimistic camp, led by firms like Bank of America and Goldman Sachs, anticipates a period of strong, sustained growth fueled by pro-growth government policies and a surge in private investment.

Key Drivers:

- “OBBBA” Fiscal Stimulus: The “One Big Beautiful Bill Act” is seen as a central pillar, extending tax breaks (Tax Cuts and Jobs Act), introducing new investment incentives, and potentially reducing tariffs.

- Deregulation: Reductions in regulatory burdens, specifically in the financial and energy sectors, are forecasted by Goldman Sachs and J.P. Morgan Asset Management to boost M&A activity and reduce overall business expenses.

- AI Investment Wealth Effect: The substantial capital expenditure by hyperscalers in AI infrastructure is a direct economic contributor. Goldman Sachs projects this spending to rise 34% to $533 billion in 2026, driving investment in construction, hardware, and energy infrastructure.

The Cautious Case: Structural Headwinds

A more measured view is held by institutions such as J.P. Morgan, Allianz, and UBS, who focus on the “friction costs” and structural limits of the new economic regime. They anticipate a slower, more volatile growth trajectory.

Key Constraints:

- Tariff Drag: Allianz argues that the costs of tariffs will function as a significant tax on consumers, counteracting the benefits of deregulation and depressing real incomes.

- Labor Supply Shock: J.P. Morgan highlights that potential “immigration crackdowns” could restrict the labor supply, thereby capping growth potential and exerting upward pressure on wages.

- “Bond Vigilante” Risk: Barclays and UBS warn that persistent, large deficits (projected at $1.8 trillion by NatWest) could trigger a negative response in bond markets, resulting in higher yields and stifling the recovery.

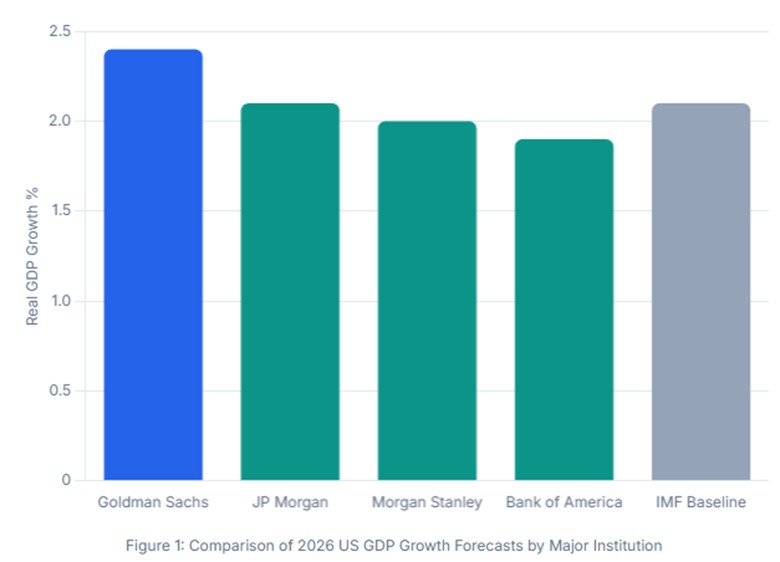

A Summary of Forecasts

United States Economic Forecasts 2026

| Institution | Real GDP Growth (2026) | Inflation Outlook (2026) | Fed Funds Rate (End 2026) | Primary Growth Drivers | Primary Risks |

| Bank of America | 2.4% (4Q/4Q) | Plateau ~3.0% | Two cuts (June/July) | Fiscal Stimulus (“OBBBA”), Deregulation | Higher rates choking growth |

| Goldman Sachs | 2.0% – 2.5% | Core PCE ~2.0% | 3.00% – 3.25% | Tax cuts, AI productivity, Ease of financial conditions | Labor market overheating |

| Morgan Stanley | 1.8% | Core PCE 2.6% | 3.00% – 3.25% | Consumer resilience, AI adoption | Immigration restrictions |

| J.P. Morgan | ~1% – 3% (Volatile) | High & Volatile (>2.5%) | 2–3 Cuts total | AI Capex, Tariff refunds | Inflation volatility, Asset bubbles |

| Wells Fargo | 2.3% | PCE 2.7% | 3.00% – 3.25% | Investment in AI, Consumer strength | Trade policy uncertainty |

| Allianz | 1.5% – 2.0% | > 3.0% (Sticky) | 3.25% – 3.50% | AI investment, Front-loaded stimulus | Stagflation, Tariff aftershocks |

| UBS | 1.7% | Moderate | Lower (Cuts expected) | “Agentic” AI, Financial conditions | Debt sustainability, Inflation |

| Barclays | Solid / Trend | 3.0% (CPI) | Modest cuts | AI spending, “OBBA” tax rebates | Wage-price spiral, Tariffs |

| Deutsche Bank | Re-acceleration | Disinflation trend | < 3.50% | Broadening growth, Tax cuts | Layoffs, Consumer spending |

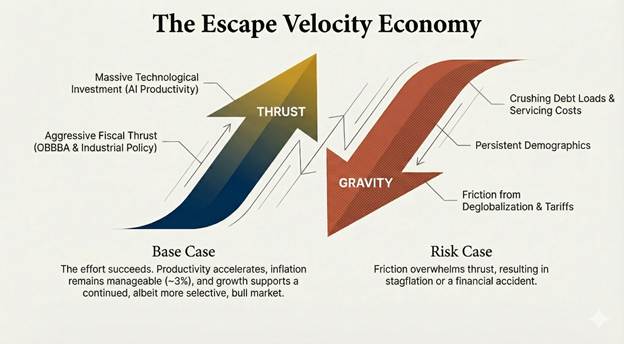

The Bottom Line

The central theme for the 2026 global economy is achieving “Escape Velocity.” The U.S. is at the forefront of this push, leveraging substantial fiscal spending and massive investment in AI and other technologies. The goal is to overcome the powerful drag exerted by high global debt levels and the trend toward deglobalization.

Core Scenarios:

- The Base Case (Success): This ambitious effort succeeds. We would see an acceleration in productivity, a stabilization of inflation near a manageable 3% target, and strengthened economic growth, all supporting a sustained bull market.

- The Risk Case (Failure): The opposing forces prove too strong. The friction costs associated with tariffs, elevated interest rates, and the burden of debt service overwhelm the growth drivers. This scenario would lead to either stagflation or a significant financial disruption.

The AI 2026 Forecast

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.