There is concern that in the wake of the pandemic the Federal Housing Administration could soon find itself in a lending crisis. This does not seem to be the case, for now. Let’s take a look at the history and purpose of the FHA and where things stand now and why.

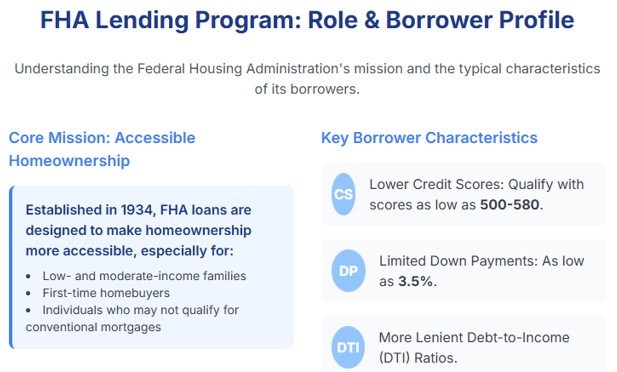

Originating in 1934, the FHA’s mission is to make home ownership a reality for first time home buyers and buyers with sub-optimal credit. This infographic explains the typical characteristics of FHA borrowers.

The Forbearance Concern

The reason for the recent concern about the solvency of FHA stems from the drastic increase in forbearance from 2019 forward. Forbearance is a form of repayment relief granted by a lender that temporarily postpones payments due from a borrower, while interest on the loan typically continues to accrue. This is obviously not a good situation and the widespread use of forbearance is not a good sign for the health of the FHA loan portfolio. Here is an infographic that illustrates the growth of forbearances from 2019 to 2024.

Cumulatively, from the start of the pandemic in March 2020 through fiscal year 2024, the FHA has granted approximately 2.7 million forbearances. This figure, reported by HUD in November 2024, underscores the significant role the agency played in providing relief to homeowners facing financial hardship.

Data for forbearances initiated in 2019, prior to the pandemic, is not readily available in public reports, which have largely focused on the period covered by the CARES Act. However, forbearance levels were significantly lower during that time.

This is a concerning trend. An interesting question is how many of the loans that are in forbearance are also delinquent? Forbearance is a temporary suspension or reduction, while delinquency is non-payment.

As of early 2025, an estimated 65,000 FHA loans are in forbearance and are also considered delinquent. This figure is derived from the latest data on FHA loan portfolios and forbearance rates, coupled with the reporting methodologies used by the mortgage industry.

According to the U.S. Department of Housing and Urban Development's (HUD) February 2025 FHA Single-Family Loan Performance Trends Report, there were a total of 7.8 million FHA-insured loans. Meanwhile, the most recent data from the Mortgage Bankers Association (MBA) in March 2025 indicate that 0.83% of Ginnie Mae loans, which are primarily composed of FHA and Department of Veterans Affairs (VA) loans, were in forbearance.

What’s Driving Delinquencies?

This infographic illustrates the FHA total delinquency rate and the total serious delinquency rate.

A 10.62% delinquency rate and a 4.79% serious delinquency rate (currently on the rise) are concerning. Especially when compared to the conventional, private sector, delinquency rates of 2.7%. That’s four times more.

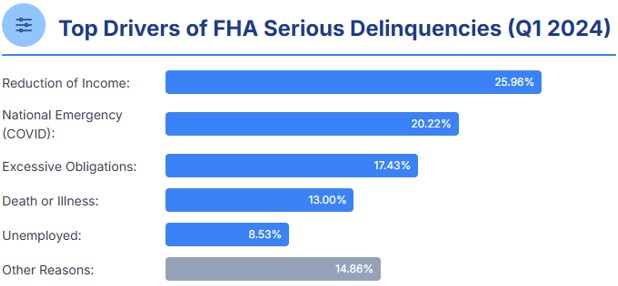

We have already established the primary driver for forbearance, the pandemic and its follow-on effects. What about the drivers for delinquencies? Take a look at this infographic.

The most interesting category is ‘Other Reasons’. What is that? It is sadly unknowable, but there is a great deal of suspicion surrounding it. I believe that a significant percentage of the 14.86% are borrowers that have the capacity to pay but are working the system and intentionally not paying. It is a cycle of forebear, pay, stop payment, go delinquent, forebear, pay, stop payment, forebear…etc. These abuses of the system are referred to as ‘strategic default’. The agencies claim it is impossible to quantify, but I have my doubts.

FHA Stress Or Systemic Crisis?

Is the system stressed or is this an actual crisis? Just with the information so far you could easily make the argument for crisis, but that does not appear to be the case. Why? The FHA is funded primarily by mortgage insurance premiums. By Congressional mandate, at least 2% of these funds are required to be held back in the FHA’s Mutual Mortgage Insurance Fund, (MMIF), to handle periods of market stress. Consider this infographic.

Currently the FHA MMIF is flush with cash. In fact, the fund has increased on a net basis since 2017 by $146B. It is believed that this abundance of cash would allow the FHA to meet any short-term needs that could result from a loan crisis. Here are some factors that argue for and against an existing crisis.

Signs of “Borrower Crisis” / Acute Stress:

- High & rising FHA delinquencies (vs. Conventional)

- FHA borrower vulnerability to economic pressures

- Expert concerns about current trajectory

- Operational weaknesses

Factors Against “Systemic FHA Crisis”

- Exceptionally strong MMIF (11.47% capital ratio)

- Overall market delinquencies below historic crisis levels

- No imminent FHA institutional collapse warning

- Serious Delinquency Rates comparable to some pre-pandemic stable periods

The Bottom Line

Significant strain exists within the FHA program due to high delinquency rates and borrower sensitivity to economic fluctuations. Despite this, the Mutual Mortgage Insurance Fund maintains a strong financial position, offering a considerable buffer. But what happens if the next crisis isn’t short lived?

There are ongoing risks and economic challenges, high borrower debt-to-income ratios, and unresolved issues in lending practices and supervision (gaming the system).

And of course, all of this does not address the housing market in general where inventories would skyrocket in the event of a crisis, depressing values and trapping underwater borrowers in negative equity situations. What is the incentive of negative equity borrowers to not walk away and thereby making the crisis worse?

Today the FHA is under stress resulting from the factors mentioned above, but not a crisis per se. At least not yet.

AI Loan Crisis!

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.