There is an energy crisis in the U.S., just not in the way you might think.

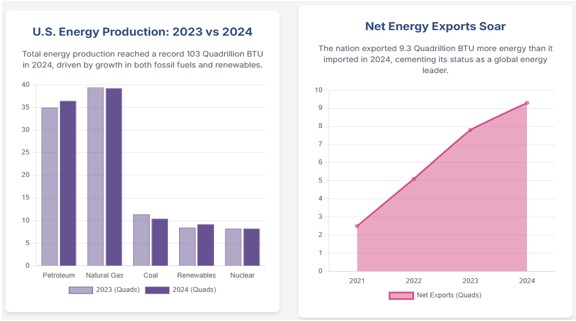

The U.S. is not experiencing an “energy production crisis.” In 2024, the nation reached record-breaking total energy production, exceeding 103 quadrillion British thermal units (quads), and became a major net energy exporter, achieving its highest surplus since 1949 (9.3 quads). This was driven by historic output in both fossil fuels (natural gas, crude oil) and explosive growth in renewables. Solar and wind production increased by 25% and 8% respectively, with solar surpassing hydropower for the first time.

However, this abundance masks a far more complex and perilous systemic crisis. The true vulnerability lies in the aging and increasingly fragile system for delivering that energy as reliable electricity. The North American Electric Reliability Corporation (NERC) warns of “rising grid reliability risks,” with “roughly half of the United States facing a high or elevated risk of energy shortfalls.” This creates a “resource adequacy” gap due to retiring dispatchable power generation (122,000 MW projected over 10 years) and declining plant performance.

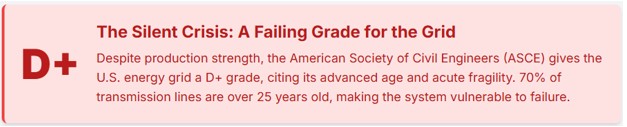

A few months back, we looked at the state of U.S. infrastructure overall, not just energy production and transmission. The American Society of Civil Engineers (ASCE) gave the U.S. power grid terrible marks. That remains the case now.

No one is talking about this let alone taking any significant action to correct this grievous situation. And that is a huge problem.

The Coming Demand Tsunami: Data Centers and Electrification

After over a decade of flat growth, U.S. electricity demand is entering a period of sustained and dramatic growth – a demand tsunami. The U.S. is staring into a consumption furnace of continuous and expanding data center and AI energy demand.

Drivers of Surging Energy Demand

The United States is facing an unprecedented surge in energy demand, driven primarily by three key factors:

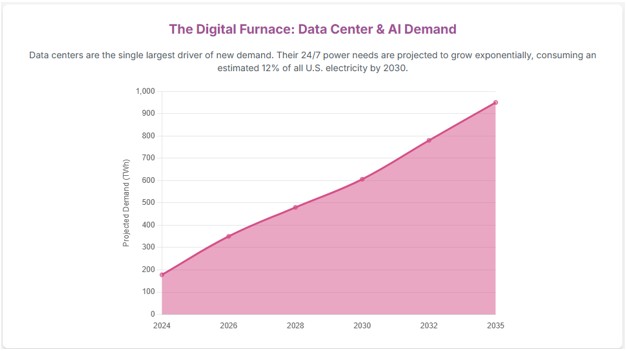

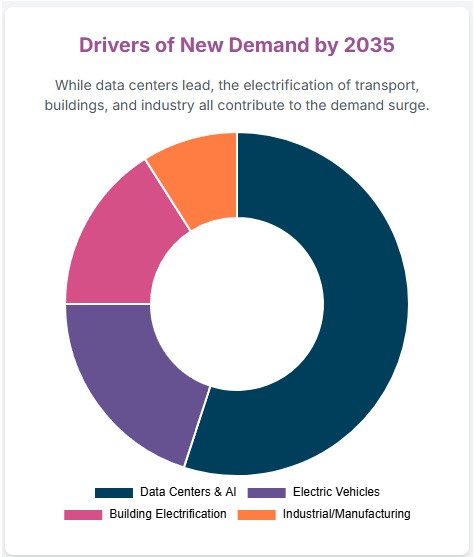

- Data Centers and AI: The most significant and immediate driver. Data center energy consumption, which accounted for 4% of total U.S. usage in 2023, is projected to triple to 12% by 2030, reaching 606 TWh and as high as 950 TWh by 2035. Some forecasts even predict a 25% increase in total U.S. electricity demand by 2030, largely due to data centers and manufacturing. These facilities operate continuously, are geographically concentrated, and experience exponential, inflexible growth.

- Electrification of Everything: Broader trends are also contributing to this demand. This includes the rapid adoption of electric vehicles (EVs), with e-mobility and charging demand projected to increase by 9,000% by 2050. Building electrification, encompassing heating, water heaters, and stoves, as well as a resurgence in domestic manufacturing, are further accelerating this trend.

- New Growth Baseline: Energy efficiency no longer offsets demand growth. Planners must anticipate significant, sustained net demand growth, requiring 80 GW of new generation capacity annually from 2025-2045—double the past five years' average.

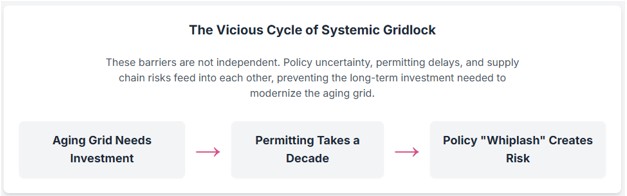

Foundational Cracks: Systemic Barriers to Meeting Demand

The ability to build a modern, reliable energy system is hampered by four barriers that create systemic gridlock.

The U.S. energy sector faces significant challenges stemming from an aging grid, a cumbersome permitting process, inconsistent policies, and new geopolitical realities.

- Aging Grid Infrastructure: As stated previously, the ASCE gave the U.S. energy sector a “D+” in 2025 due to an electric grid where 70% of transmission lines and large power transformers are over 25 years old. This outdated infrastructure leads to increased outages, inefficiencies, and cyber vulnerabilities. Modernization is projected to cost hundreds of billions of dollars, with a potential investment gap of $702 billion by 2033.

- Permitting Quagmire: Slow, complex permitting severely hinders energy infrastructure development, taking 4-5 years for power plants and up to 29 years for critical mineral mines from discovery to production. Legal challenges add an average of four more years.

- Policy Pendulum and Investment Uncertainty: Frequent shifts in energy policy between presidential administrations create an unstable and high-risk environment for investors.

- New Geopolitics of Energy: From Oil to Minerals: Energy security hinges on critical mineral and energy supply chains, dominated by rivals like China. China's control over mineral processing (rare earth elements, lithium, cobalt, graphite) and manufacturing of solar panels and batteries grants it significant geopolitical leverage. EVs demand six times more mineral inputs than gasoline cars, projecting a 6-21x increase in key mineral demand by 2040.

Forging the Future: A Portfolio of Solutions

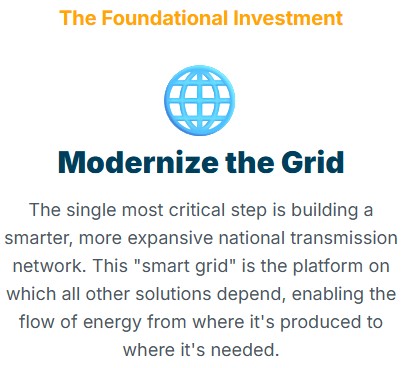

Addressing the energy paradox requires a multi-faceted approach, not a single solution. This strategy must combine fundamental grid upgrades with a diverse portfolio of generation and storage technologies.

Key Investment Areas:

- Grid Modernization: This is the most crucial investment. It entails developing a smarter and more expansive network equipped with advanced sensors and AI. This also involves implementing Grid-Enhancing Technologies (GETs) for immediate capacity increases and a significant expansion of the high-voltage transmission network to facilitate renewable energy integration and improve interregional reliability.

- Dispatchable, Clean, and Firm Power: These resources are vital for ensuring grid reliability when variable renewable sources are not producing.

- Energy Storage: Battery energy storage systems (BESS) offer the most flexible and rapid-response dispatchable resource, enabling energy arbitrage and critical grid stability services. Utility-scale storage capacity is projected to more than double by 2026.

- Small Modular Reactors (SMRs): Advanced nuclear SMRs provide large-scale, carbon-free, firm power. Their smaller size and scalability make them ideal for powering large data centers.

- Geothermal and Hydropower: Enhanced Geothermal Systems (EGS) can significantly broaden the geographical areas where geothermal power is feasible, boasting an exceptionally high-capacity factor exceeding 92%. Hydropower potential can be unlocked by upgrading existing facilities, electrifying the 97% of U.S. dams that currently lack power generation capabilities, and expanding pumped storage hydropower (PSH).

- Scaling Variable Renewables: Solar and wind lead new generation growth, but their variability demands significant investment in transmission, forecasting, and firming resources.

- Enduring Role of Natural Gas: Natural gas remains and will likely continue to be in the near future, the foundation of the U.S. electricity system, accounting for 43% of electricity generation. It is considered an essential 'bridge' or 'reliability' fuel due to its dispatchability.

The Bottom Line

The U.S. energy system is at a critical juncture, presenting a unique opportunity for significant transformation. While technological solutions are readily available, the primary hurdles lie in institutional implementation and overcoming the resistance from outdated systems and political fragmentation. Achieving national agreement on a modern, robust energy system is essential. The future of American economic competitiveness and national security in the 21st century hinges on this effort.

The AI Energy Solution

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.