On September 17, 2025, the Federal Open Market Committee (FOMC) began a monetary easing cycle by lowering the target range for the federal funds rate by 25 basis points, setting it at 4.00%−4.25%. This marks the first rate reduction of 2025, following a pause in the first half of the year and 100 basis points of cuts in Q4 2024. Federal Reserve Chair Jerome Powell stated that this decision was a risk management measure, primarily in response to a significant decline in the U.S. labor market, despite ongoing high inflation.

The September Decision, A Targeted Easing

The FOMC lowered the federal funds rate target by 25 basis points to 4.00%–4.25%. This marks the first rate cut of 2025, reversing a previous restrictive stance. Governor Stephen I. Miran dissented, advocating for a more aggressive 50-basis-point reduction, highlighting internal debate on the appropriate response speed and magnitude.

Complementary adjustments were made to administered rates, with interest on reserve balances lowered to 4.15% and the primary credit rate (discount rate) to 4.25%.

Despite the rate cut, the FOMC affirmed its commitment to continue reducing its holdings of Treasury securities and agency debt along with mortgage-backed securities. This signifies the continuation of quantitative tightening (QT), with monthly reductions of up to $60 billion in Treasury securities and $35 billion in agency mortgage-backed securities.

This simultaneous rate cut (easing) and continuation of QT (tightening) indicate a somewhat dichotomous overall policy stance. The rate cut is a targeted, tactical adjustment aimed at managing specific near-term risk, namely, the deteriorating labor market outlook—while the commitment to ongoing balance sheet normalization signals a concern for inflationary pressures.

Economic Rationale or Why Now?

The Federal Reserve's recent policy pivot was primarily driven by a significant and rapid deterioration in the U.S. labor market. This decision was made despite an elevated inflationary environment, indicating a risk management framework that prioritizes the trajectory of employment indicators over the absolute level of inflation.

Deteriorating Labor Market – The Primary Catalyst:

- Shift in Risk Assessment: The FOMC formally acknowledged that downside risks to employment have risen, a notable change from its solid assessment in July 2025.

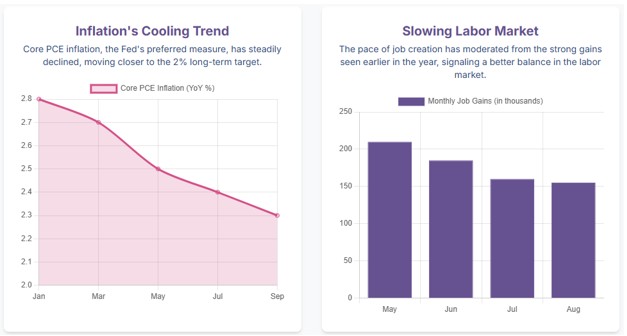

- Sharp Deceleration in Payroll Growth: Over the preceding three months, payroll job gains averaged only 29,000 per month, which is substantially below most estimates of the breakeven rate needed to keep unemployment stable.

- Rising Unemployment Rate: The unemployment rate increased to 4.3% in August.

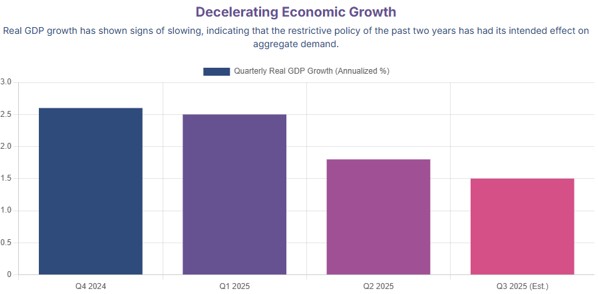

- Moderating Economic Activity: Real GDP growth slowed to an annualized pace of approximately 1.5% in the first half of 2025, a decrease from 2.5% in the previous year, mainly due to a moderation in consumer spending.

Challenging Inflationary Environment (Despite Rate Cut):

- Persistent Price Pressures: Total Personal Consumption Expenditures (PCE) prices rose by 2.7% over the 12 months ending in August 2025, with core PCE increasing by 2.9%. Both figures are nearly a full percentage point above the Fed's 2% target.

- Tariff Uncertainty: Chair Powell noted that government tariff policies had started to increase prices and contributed to rising near-term inflation expectations. This raised questions about whether these were one-time shifts in the price level or a persistent inflationary issue.

Risk Management Framework:

The Fed's preemptive action was a calculated choice: to act preemptively based on the deteriorating trajectory of the labor market, thereby accepting the risk of a more prolonged period of above-target inflation. This highlights a greater sensitivity to the rate of change in employment indicators than to the absolute level of inflation.

Forward Guidance and Projected Policy Trajectory

The Federal Reserve's recent Summary of Economic Projections (SEP) and Dot Plot reveal a cautious approach to monetary policy, signaling a slow-motion easing cycle while emphasizing data dependency.

Economic Projections (SEP):

- Real GDP Growth: Projections for 2025 have been slightly raised to 1.6% (from 1.4% in June), indicating an anticipation of below-trend growth but not a recession.

- Unemployment Rate: The unemployment rate is expected to reach 4.5% by the end of 2025, followed by a gradual decline.

- Inflation Outlook: Total PCE inflation is projected at 3.0% for 2025, decreasing to 2.6% in 2026 and 2.1% in 2027. The Fed does not anticipate inflation returning to its 2% target until 2028.

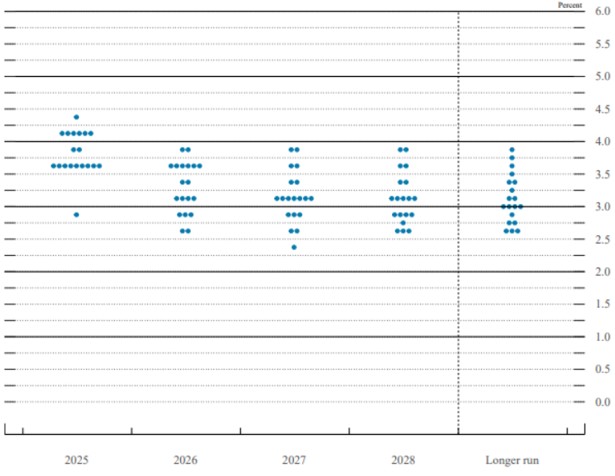

Projected Interest Rate Path (Dot Plot):

- Two More Cuts in 2025: The median projection for the federal funds rate at the end of 2025 is 3.6%, suggesting two additional 25-basis-point cuts in October and December.

- Gradual Easing: The projected trajectory indicates a slow-motion easing cycle, with the median rate falling to 3.4% by the end of 2026 and 3.1% by the end of 2027. This gradual approach is attributed to the persistent pressure from elevated inflation.

- Divergent Views: The dot plot highlights significant disagreement among policymakers, with projections ranging from no further cuts to an additional 125 basis points of easing by year-end, underscoring a high degree of uncertainty.

Chair Powell's Communication:

Chair Powell reiterated that monetary policy is not on a preset course, emphasizing that future decisions will be made on a meeting-by-meeting situation and are strictly data-dependent, thereby maintaining flexibility.

The Bottom Line

The Federal Reserve's September 2025 rate cut was a proactive, risk-management decision, prioritizing potential labor market downturns over persistent inflation. The FOMC projected slow, shallow, and protracted easing cycle highlights the challenge of balancing these concerns.

The effectiveness of this strategy hinges on future economic developments. It's a significant gamble on the stability of inflation expectations and the adaptability of the labor market. A soft landing, characterized by controlled inflation and stable employment, would validate the policy. However, a significant decline in employment or a resurgence of inflation would indicate a significant policy error, leaving the Fed in a more precarious position. The path ahead is fraught with uncertainty and offers no risk-free options.

The AI Dot Plot

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.