This week’s highlights…

- Wall Street is debating whether the current AI investment trend is a sustainable productivity boom or a potential historic bubble.

- Tech giants are investing record-breaking capital into AI infrastructure, such as chips and data centers.

- Halbert Wealth Management emphasizes that navigating this investment cycle requires balancing technological optimism with financial reality.

Profitability and the Cashflow Squeeze

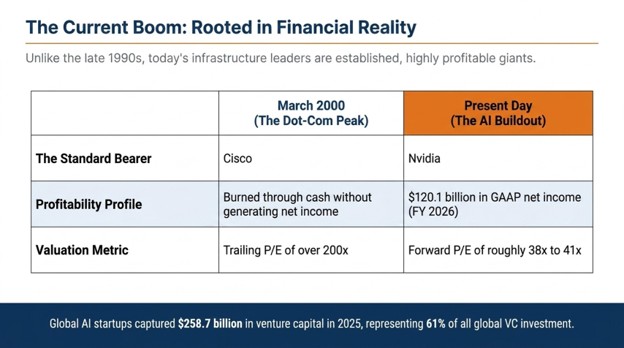

Unlike the late 1990s dot-com bubble, where many tech darlings burned through cash without generating net income, today’s infrastructure leaders are established, highly profitable giants. For example, accelerated computing kingpin Nvidia reported a staggering $120.1 billion in GAAP net income for fiscal year 2026. It currently trades at a forward P/E ratio of roughly 38x to 41x, a far cry from Cisco’s trailing P/E of over 200x at its March 2000 peak.

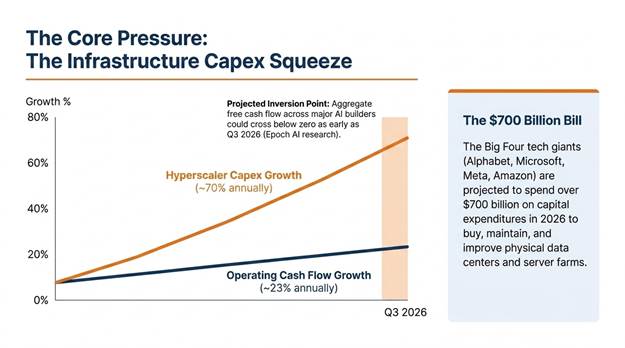

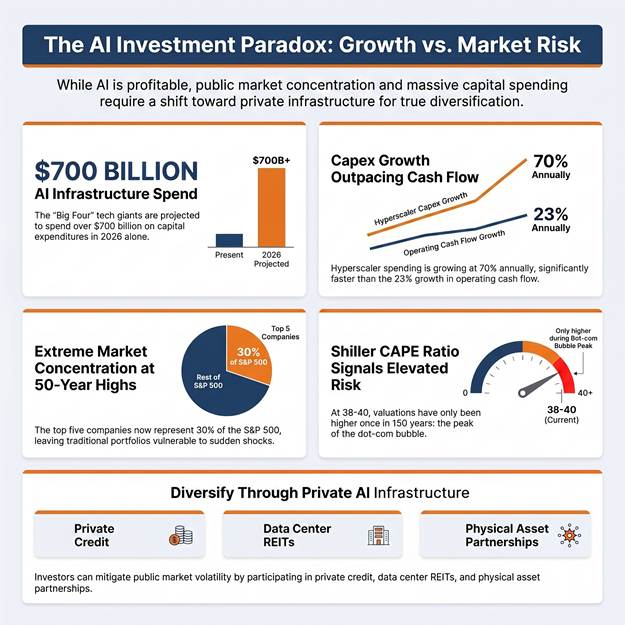

However, the sheer velocity of this buildout is putting intense pressure on corporate cash reserves. Globally, AI startups captured $258.7 billion in venture capital in 2025, representing 61% of all global VC investment. At the corporate level, the “Big Four” tech giants, Alphabet, Microsoft, Meta, and Amazon, are projected to spend over $700 billion on capital expenditures (capex) in 2026. In plain terms, capex simply refers to the cash spent to buy, maintain, or improve physical assets like data centers and server farms.

According to research from Epoch AI, hyperscaler capex is growing at roughly 70% annually against operating cash flow growth of just 23%. Under this model, aggregate free cash flow across major AI builders could cross below zero as early as Q3 2026. We are already seeing this pressure: in Q1 2026, Amazon’s operating cash flow was $26.0 billion against $44.2 billion in capex, dragging down its free cash flow and increasing long-term debt to $119.1 billion.

Market Concentration and Volatility Risks

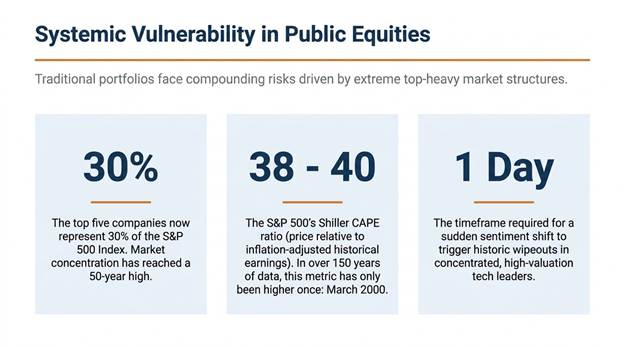

Another alarming signal is market concentration, which has reached a 50-year high. The top five companies now represent 30% of the S&P 500 Index. Furthermore, the S&P 500’s Shiller CAPE ratio, measuring stock prices relative to historical earnings adjusted for inflation, currently stands at an elevated 38 to 40. In over 150 years of data, this metric has only been higher once: during the peak of the dot-com bubble in March 2000.

This top-heavy structure leaves traditional portfolios highly vulnerable to sudden sentiment shifts. We saw this fragility in action during the “DeepSeek shock” of January 27, 2025, when a competitive, low-cost AI model release wiped a record-breaking $588.8 billion from Nvidia’s market value in a single day.

At Halbert Wealth Management, our absolute-return, risk-aware philosophy prompts us to navigate these concentrated waters with extreme care. We help clients build resilient, diversified portfolios that incorporate non-traditional and non-correlated strategies to smooth out public equity volatility and manage downside risk.

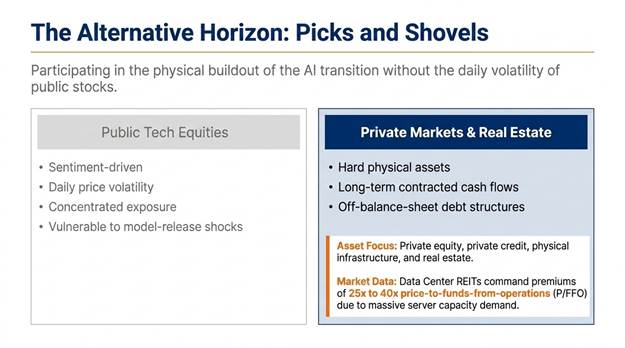

Relying solely on traditional public equity indices exposes investors to the direct price whipsaws of highly concentrated tech giants. What many investors overlook is that the physical buildout of the AI revolution is opening up compelling opportunities in the private markets, specifically through alternative assets, private equity, private credit, physical infrastructure, and real estate.

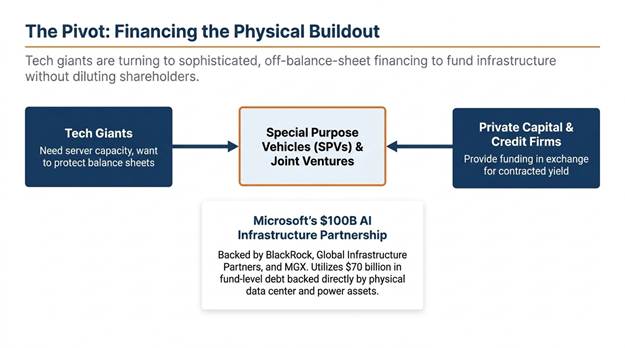

To fund this massive buildout without diluting shareholders or stretching their balance sheets, tech giants are turning to sophisticated, off-balance-sheet financing structures. They are increasingly partnering with private equity and private credit firms to establish joint ventures and special purpose vehicles (SPVs). For example, Microsoft’s $100 billion AI Infrastructure Partnership, backed by BlackRock, Global Infrastructure Partners, and MGX, utilizes $70 billion in fund-level debt backed directly by physical data center and power assets.

Additionally, real estate plays a critical role. The massive demand for server capacity has turned Data Center REITs (Real Estate Investment Trusts) into premium, income-generating assets, with top-tier players commanding multiples of 25x to 40x price-to-funds-from-operations (P/FFO).

By selectively participating in these private market channels, risk-aware investors can focus on the physical “picks and shovels” of the transition, benefiting from long-term contracted cash flows and hard real estate assets, without the daily volatility of public stocks. Please keep in mind that alternative assets carry risk, are not guaranteed, and past performance is not a guarantee of future returns.

Ready to learn more?

We have put together a detailed, client-centric: "Alternative Assets Explainer" This guide breaks down the alternative asset landscape and explains these institutional style strategies.

Request your complimentary copy today.

You can also schedule a brief, no-obligation consultation to review your current portfolio diversification strategy.

Infographic Summary

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.