It's unusual to see disagreement at the Fed, especially from someone who thinks they should be less aggressive. But when it happens, it's a big deal. Even though it doesn't happen often, these disagreements often hint at future changes and push against the Fed's tendency to stick with the status quo.

History shows the Fed often reacts too late, partly because policies take time to show their effects, decisions are made by committee, and they're more worried about acting too soon than too late. So, it's really important to encourage thoughtful disagreement to make sure monetary policy is more flexible and effective.

Dissenting votes at the Fed are pretty rare, happening in only 6% of votes between 1957 and 2013. When they do happen, it's usually a “hawkish” dissent, meaning they wanted tighter monetary policy (249 times) rather than an “easier policy” or “dovish” dissent (160 times). This makes those dovish dissents especially interesting.

Here's a breakdown of who dissents and how:

- Board of Governors members are way more likely to dissent for easier policy, making up 78% of all those dovish dissents.

- Regional Federal Reserve Bank Presidents tend to dissent more for tighter policy, accounting for 72% of hawkish dissents.

Fed Governors, who are appointed by the President, care more about jobs, while Presidents, appointed by local boards, focus more on keeping prices stable.

The Fed often gets flak for being slow to react. Historically, they tend to keep interest rates low for too long, letting inflation get out of hand. Then they wait too long to raise rates, which can lead to recessions. You can see this pattern in both times they tightened policy, like the Great Inflation from 1965-1982, and when they eased it, like the Global Financial Crisis.

A few things contribute to this slowness:

- Lagged effects: Monetary policy is slow to take effect, so policymakers are cautious.

- Consensus-driven: The Federal Open Market Committee (FOMC) tries to reach an agreement, which can slow things down. A strong Fed chair can also make it harder for dissenting opinions to be heard.

- Fear of being wrong: Policymakers might be more worried about cutting rates too aggressively and causing inflation than waiting too long and causing a recession, which they can often blame on outside factors.

The Global Financial Crisis, Devastating Groupthink

The 2008 Global Financial Crisis is a prime example of a big failure in monetary policy, largely because a strong, widespread agreement prevented important dovish dissents from being voiced.

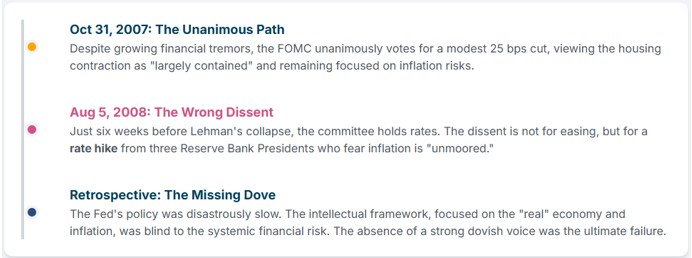

Misdiagnosis and Flawed Framework: In 2007, the FOMC mistakenly prioritized inflation risks, dismissing the escalating housing contraction as “largely contained.” Their existing macroeconomic models failed, leaving the FOMC blind to the looming catastrophe.

Hawkish Dissent in 2008: The committee's analytical blunder happened on August 5, 2008. Just six weeks before Lehman Brothers failed, three Reserve Bank Presidents—Fisher, Evans, and Plosser—disagreed, pushing for a 25 basis point rate hike. This shows that the discussion was about tightening policy, not loosening it, meaning the committee wasn't just behind the curve; it was pointed in the wrong direction entirely.

Retrospective Analysis: The Federal Reserve's response to the crisis was disastrously slow. The core issue was not a lack of individual dovish voices, but rather an institutional and intellectual environment that prevented such voices from emerging. Boston Fed President Eric Rosengren emerged as a lonely voice of concern in the aftermath of Lehman's collapse, highlighting the significant impact on the real economy.

The Tariff Slowdown and the 2025 Dissents

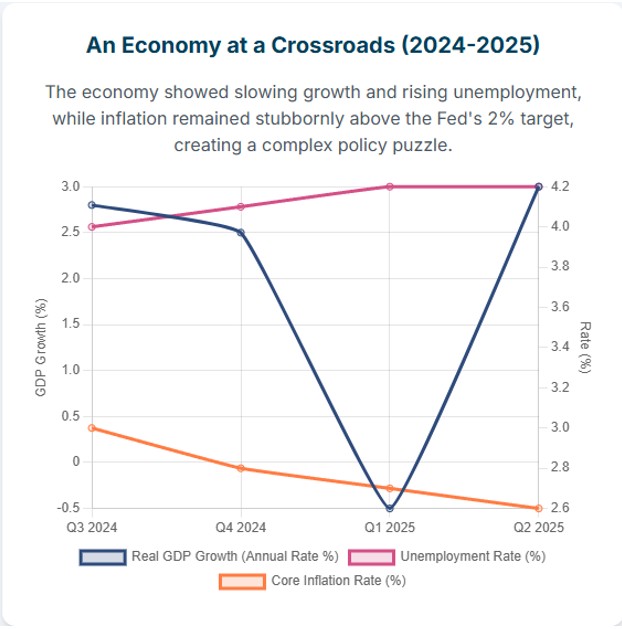

Economic Crossroads: Entering 2025, the U.S. economy faced uncertainty, with solid but decelerating growth (2.8% in 2024, contracting 0.5% in Q1 2025 before rebounding in Q2), stubborn inflation (2.5-3.0%), and significant uncertainty from new trade tariffs.

Waller-Bowman “Preemptive Strike”: At the July 30, 2025 meeting, Governors Christopher Waller and Michelle Bowman issued a historically significant dissent, voting for an immediate 25 basis point rate cut, the first time two Governors dissented on policy since 1993.

Waller's Rationale: Explicitly preemptive, arguing the Fed should cut rates to “forestall a weaker economy and a rise in unemployment,” rather than waiting for visible deterioration.

Bowman's Evolution: Notably, Bowman had dissented hawkishly in September 2024, preferring a smaller rate cut, but by July 2025, her assessment shifted, citing contained inflation pressures and the need to support the economy.

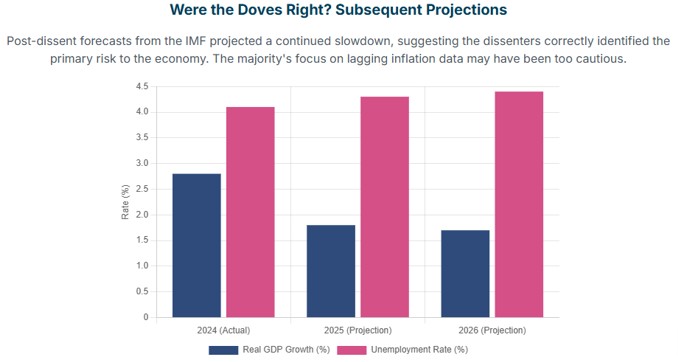

Retrospective Evaluation: The dissenters appear to have been correct. While the majority cited “elevated uncertainty” and persistent inflation, subsequent forecasts (e.g., IMF projecting deceleration to 1.8% in 2025 and 1.7% in 2026) “lent credence to the dissenters' concerns.” Their call for a preemptive “insurance” cut was the more prudent course of action.

The Value of Dissent

- An Early Warning System: Dissent is like an “informational signal” that can predict future policy actions, suggesting those who disagree often spot economic trends or risks the majority misses.

- Boosting Openness and Accountability: When people disagree, they have to publicly explain their differing views, which makes policy discussions richer and holds everyone more accountable.

- Fighting Groupthink: The Global Financial Crisis showed that the Fed's biggest risk isn't a close vote, but everyone agreeing on a bad policy. Dissent is a crucial institutional antidote to dangerous groupthink. Recent disagreements show it's normal and important to challenge the status quo and really think through risks.

The Bottom Line

Historically, Federal Reserve dissenters favoring looser monetary policy have often proven insightful, highlighting overlooked risks. The Fed should embrace this as a sign of strength. Actively valuing diverse viewpoints is crucial for a robust monetary policy framework. Fostering open debate leads to more considered decisions and greater adaptability. Respecting dissenting opinions allows the Fed to identify pitfalls, anticipate economic shifts, and formulate effective policies. But don’t expect this to alter the Fed’s trajectory. A two governor dissent is significant though not enough to derail Powell.

AI Fed Governor

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.