Private Equity & Hedge Funds Vs. Buy and Hold? No. All Three For A Better Portfolio

The investment landscape is evolving, moving from an era of low interest rates and disinflation to one of healthier foundations with potentially higher rates and greater inflation volatility. In this environment, strategically allocating to alternative assets becomes critical for enhancing returns and improving diversification beyond a traditional 60/40 portfolio. While alternative assets offer significant benefits, they also introduce challenges such as illiquidity, complexity, opacity, and substantial fees, requiring informed manager selection and due diligence.

Public Market Benchmark: The S&P 500

When people refer to “the market” the S&P 500 is it.

The S&P 500 has historically been a powerful engine for wealth creation, delivering an average annual return of over 10% since 1957.

The S&P 500 demonstrates varied historical performance across different timeframes, with returns notably impacted by significant economic events.

Historical Performance (Total Return, Annualized):

- 5-Year: 16.3% (11.33% inflation-adjusted)

- 10-Year: 12.57% (9.25% inflation-adjusted)

- 20-Year: 10.36% (7.63% inflation-adjusted). This period's lower return is notably influenced by the 2008 Global Financial Crisis (GFC).

Volatility: A fundamental characteristic of a liquid and transparent market, S&P 500 returns exhibit significant year-to-year volatility. Annual total returns show substantial dispersion (the range of returns), from a high of +31.49% in 2019 to a low of -37.00% in 2008.

Evolving Risk Profile: The S&P 500's risk profile has shifted, with increasing concentration risk becoming a prominent factor. So far in 2025, the “Magnificent 7” technology firms alone constitute over 30% of the index. This structural change underscores the growing importance of diversification within investment strategies.

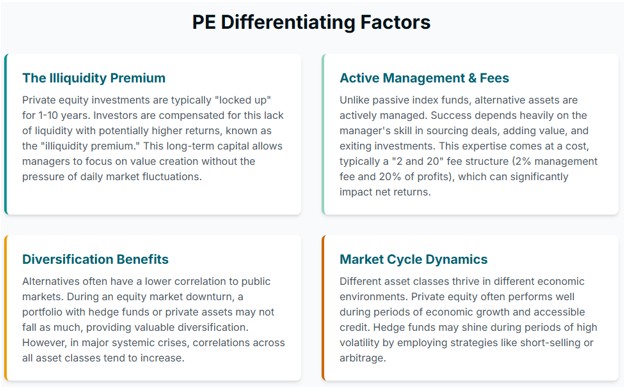

Private Equity: The Pursuit of Alpha and the Illiquidity Premium

Private Equity (PE) is defined by active management and a long-term investment strategy. These investments are more available to retail investors now than at any other time.

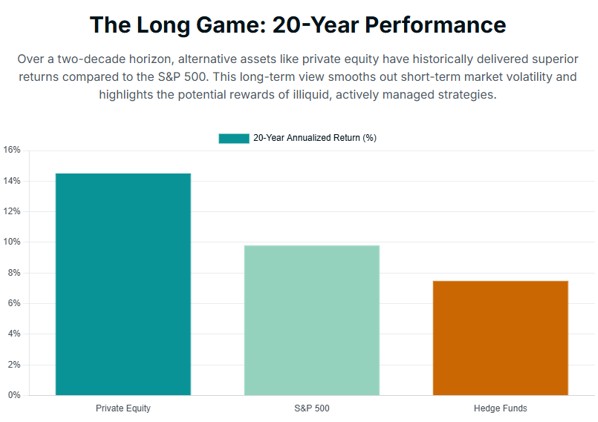

Data from Cambridge Associates LLC U.S. Private Equity Index (Net of fees through 2024) demonstrates a history of strong returns:

- 5-Year Annualized Return: 16.98%

- 10-Year Annualized Return: 16.28%

- 20-Year Annualized Return: 15.01%

This persistent return advantage, known as alpha, is the principal reason investors are willing to accept the significant fees and illiquidity inherent in the asset class.

Understanding PE Returns

The Measurement Challenge: A direct comparison between PE's Internal Rate of Return (IRR) and a public index's Compound Annual Growth Rate (CAGR) can be misleading due to sensitivity to timing. The Public Market Equivalent (PME) methodology offers a more accurate comparison.

PE funds can have some or all these characteristics.

- Operational Value Creation: A hands-on approach to improving portfolio companies.

- Strategic Use of Leverage: Utilized to amplify equity returns.

- Long-Term Horizon: Allows for strategic changes over 10+ years, free from the immediate pressures of public markets.

- Sector and Size Exposure: Provides access to a vast universe of private companies, often smaller and in niche sectors.

- Illiquidity Premium: Compensation received for “committing capital for long, uncertain periods during which it cannot be easily accessed.”

The Reality of Risk in Private Equity

Volatility Mirage: The often-reported low volatility of PE is often misunderstood. This is due to infrequent, appraisal-based valuations (mark to market) that artificially smooth the reported return series. When adjusted, the true volatility of some PE can be comparable to, or even higher than, that of public equity.

Hedge Funds: Uncorrelated Returns and Downside Protection

Hedge funds are a highly diverse category seeking returns less dependent on traditional markets. Comparing hedge fund performance to the S&P 500 reveals a nuanced story over different time horizons, highlighting the importance of considering various factors beyond simple aggregate returns.

Aggregate Performance

While hedge funds may lag in robust bull markets, their relative performance improves over longer periods that include volatile market conditions. Their core value proposition lies in providing a distinct, more resilient return stream throughout a complete market cycle.

The Criticality of Strategy Dispersion

It is a common yet significant analytical error to treat “hedge funds” as a singular asset class. Key strategy groups, such as Equity Hedge, Event-Driven, Global Macro, and Relative Value, each possess unique risk/return profiles. Therefore, allocation decisions should be made at the individual strategy level, not for “hedge funds” as a whole.

Performance Across Different Market Types

The true utility of hedge funds becomes apparent during specific macroeconomic conditions. Since 1990, the HFRI Composite Index has notably outpaced the 3.4% from public equities during periods of above-average inflation. Similarly, hedge funds have outperformed in periods characterized by more 'normal' interest rates. This suggests that their value is tactical and conditional on the prevailing economic environment.

The Bottom Line

With the era of zero-bound interest rates coming to a close, it is important to reevaluate portfolio composition.

Key drivers in this environment include:

- Fiscal Activism & Higher Inflation: This presents a structural tailwind for real assets like real estate and infrastructure, as well as Global Macro hedge funds.

- Artificial Intelligence (AI): AI creates opportunities for growth in both Private and Public Equity funds. Private market managers are particularly well-positioned to generate alpha by implementing AI within their portfolio companies.

- Energy Transition & Deglobalization: This represents a generational opportunity for private capital (private equity, private credit, and infrastructure), particularly in areas such as renewable energy, logistics, and advanced manufacturing.

In this shifting landscape, active management and the ability to access unique sources of alpha and diversification will be crucial. Therefore, a thoughtfully constructed and dynamically managed allocation to alternative investments alongside more traditional public equity will be an indispensable tool for building resilient, high-performing portfolios.

Alternative Investment AI

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.