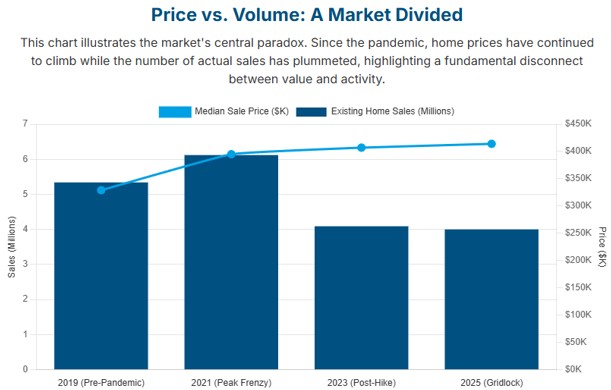

A Picture of Gridlock

The market is defined by a core contradiction: record-high prices coexist with historically low sales activity. This isn’t a normal cycle; it’s a market frozen in place.

The housing market currently faces a policy-driven deadlock, presenting a mixed scenario of stable prices alongside weak sales and an unusual inventory situation.

Despite a considerable decrease in sales activity, home prices have displayed unexpected stability, resisting predictions of a sharp decline. In April 2025, the national median existing-home price reached a record $414,000 for that month, marking the 22nd consecutive month of year-over-year increases. This signifies a substantial 27% increase since the first quarter of 2020.

While prices remain elevated, the pace of their increase has slowed. Analysts anticipate modest average growth of approximately 2% for 2025, with numerous local markets experiencing little to no change.

Elevated mortgage rates have caused a housing market standstill, with existing-home sales significantly below pre-pandemic figures in April 2025 despite a robust labor market. A declining Pending Home Sales Index indicates this trend will persist. New single-family home sales saw a rise in the same period, driven by builder incentives and comparable pricing with existing homes, highlighting builder competition.

This is the current housing market paradox, a disconnect between value and activity. The below infographic illustrates this unusual situation.

While headline inventory figures suggest a market recovery, a closer look reveals a concerning affordability crisis.

Overall Inventory Growth: In April 2025, total for-sale inventory reached 1.45 million units (a 4.4-month supply), marking 18 consecutive months of growth and a nearly 20% year-over-year increase in March 2025.

Affordability Disparity: This inventory growth disproportionately favors higher-income buyers. In March 2025, only 21.2% of listings were affordable for households earning $75,000-$100,000—a “catastrophic drop” from 48.8% in 2019. The situation is even more dire for those earning under $50,000, with only 8.7% of listings within their reach.

Middle-Income Housing Shortage: The market is experiencing a significant shortage of approximately 416,000 listings priced at or below $255,000, the benchmark for middle-income affordability. This underscores the growing divide between available inventory and what a substantial portion of the population can actually afford.

Regional Market Divergence

The U.S. housing market in 2025 is displaying increasing divergence across regions, largely due to variations in local housing supply.

Regions with constrained supply, such as the Northeast and Midwest, are experiencing more competition among buyers. This translates to quicker sales and more stable price appreciation.

Conversely, the South and West regions, especially areas that saw rapid growth during the pandemic, are witnessing a significant rise in housing inventory. In April 2025, active listings surged by 41.7% year-over-year in the West and 33.3% in the South.

This rebalancing is evident in Travis County, Texas (Austin). As of May 2025, the median sale price there has decreased by 4.5% compared to the previous year, settling at $525,000. Homes are also staying on the market longer, averaging 50 days before sale, and are selling for approximately 2.6% less than the initial list price. The available housing inventory in the area has increased considerably.

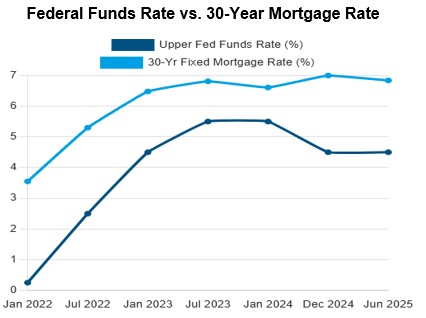

Monetary Policy as the Market's Architect

The Federal Reserve’s aggressive rate-hike cycle, designed to combat inflation, was the primary trigger for the current market state. As the Fed Funds Rate soared, mortgage rates followed in lockstep, crushing affordability.

The Fed's Rate Adjustments (2022-2025)

- Aggressive Rate Hikes (2022-2023): From March 2022 to July 2023, the FOMC raised the federal funds rate eleven times, reaching a peak of 5.25%-5.50%.

- Subsequent Easing (Late 2024): By mid-2025, the federal funds rate remained stable at 4.25%-4.50% following 100 basis points of Fed rate cuts in late 2024 (September, November, December).

Impact on Mortgage Rates and Affordability

The Fed's policies directly influence mortgage rates, leading to increased borrowing costs.

- Surging Mortgage Rates: In June 2025, the average 30-year fixed mortgage rate remained high at 6.84%, despite recent Fed easing, after rising from below 3% during the pandemic to over 7% in late 2022.

- Decreased Affordability: Rising mortgage rates have sharply decreased housing affordability. A $300,000 loan's principal and interest payment at 7% ($1,996) is much higher than at 3% ($1,265).

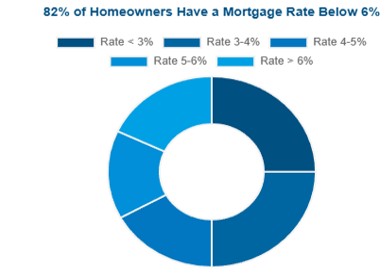

The “Golden Handcuffs” and Market Gridlock

Why isn’t inventory recovering? Millions of homeowners are “locked into” historically low mortgage rates. Selling and buying a new home would mean trading a cheap loan for an expensive one, creating a powerful disincentive to move.

A key factor sustaining high home prices and causing market stagnation is the “golden handcuffs” effect.

- Prevalence of Low-Rate Mortgages: By late 2024, an estimated 82% of outstanding mortgages had rates below 6%, with 25% below 3%.

- Disincentive to Sell: Homeowners with these low rates face a significant financial disincentive to sell and take on a new mortgage at current higher rates.

- Constrained Supply: This lock-in effect is the primary reason for the limited number of existing homes available for sale, artificially inflating prices despite weakened buyer demand.

Future Policy and Market Outlook

The trajectory of the housing market is closely tied to future Federal Reserve policy decisions.

- Persistent Elevated Rates: Most forecasts predict 30-year mortgage rates will remain between 6% and 7% for the rest of 2025, with some anticipating rates above 6.5% until 2027.

- Delicate Balance: While lower mortgage rates are needed to stimulate sales, a significant drop could also trigger renewed buyer competition and potentially lead to another period of rapid price increases.

Why 2025 Is Not 2008

Fears of a 2008-style crash are widespread but misplaced. Today’s market fundamentals are drastically different. The risk isn’t a financial collapse; it’s a severe, structural affordability crisis.

Strong Fundamentals Protect Against Financial Crash

Unlike the pre-2008 period of loose lending, today's mortgage market is strong due to stricter post-Dodd-Frank regulations and highly qualified borrowers. Homeowners have record equity (nearly $34.5 trillion in Q1 2025), and the average loan-to-value ratio is low at roughly 28%, providing a significant buffer against foreclosures unlike 2008. In contrast to the 2008 oversupply, the current market faces a chronic housing deficit of nearly 4 million homes, supporting prices and making a broad price collapse unlikely.

In 2025, the U.S. housing market faces a severe affordability crisis impacting household stability. Nearly 75% of households cannot afford a median-priced new home, which requires an income over $141,000. There's a 7.1 million unit shortage of affordable rentals for extremely low-income renters. Housing access is increasingly unequal; those earning $50,000 can afford less than 9% of listings, while those earning $200,000+ can afford 80%-100%, exacerbating the wealth gap.

Outlook for 2026 and Beyond

The path forward will be a gradual rebalancing. Don’t expect a price collapse. Instead, look for moderating price growth, slowly rising sales, and a gradual easing of the gridlock as the market adapts to the new normal.

A Fundamental Shift in Housing Demand

The rise of remote and hybrid work models represents a long-lasting structural change significantly impacting the housing market. This shift is identified as a major factor, accounting for over half of the substantial 23.8% surge in U.S. home prices between December 2019 and November 2021.

Current expectations suggest a continued, gradual stabilization of the market. US home price growth is slowing significantly, with Fannie Mae predicting a 2.78% average increase in 2026 and Zillow forecasting a slight national decrease (0.9%-1.7%) from mid-2025 to mid-2026. Regional variations, especially in some Sun Belt markets, will be significant. Mortgage rates are expected to remain around 6.0% through 2026, with no substantial reductions anticipated. Existing-home sales are predicted to rise by 13% in 2026 (NAR), and the market is projected to become balanced or favor buyers (6-7+ months of supply) between mid-2026 and mid-2027.

AI Housing Market

[Spencer]

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.