This week’s highlights…

- A detailed look into the U.S. consumer and capital spending engines

- Key U.S. GDP and inflation forecasts from the street’s top investment banks

- How non-traditional strategies can help preserve your purchasing power in a structurally higher inflation regime

U.S. GDP: Delayed, Not Denied

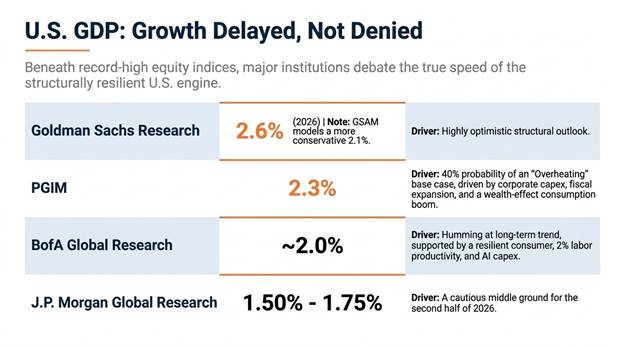

Beneath the surface of record-high equity indices lies a fascinating economic divergence. While geopolitical friction and energy shocks have caused global growth projections to be revised slightly downward, the U.S. economy continues to exhibit unique structural resilience.

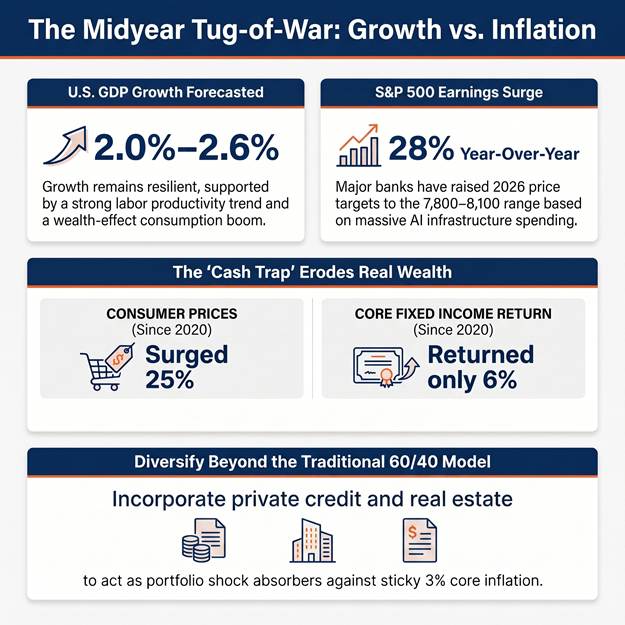

Major Wall Street institutions are currently debating just how fast the U.S. engine will run. BofA Global Research Head of U.S. Economic Research Aditya Bhave notes that U.S. growth is humming along right around its trend of “2%, give or take,” supported by a highly resilient consumer and an ongoing artificial intelligence capital expenditure boom. This view of structural health is echoed by BofA’s productivity data, which shows U.S. labor productivity trending at a solid 2%.

Meanwhile, Goldman Sachs research economists are even more optimistic, projecting U.S. real GDP growth of 2.6% for 2026, while Goldman Sachs Asset Management models a slightly more conservative 2.1%.

Taking a more cautious middle ground, J.P. Morgan Global Research expects U.S. growth to settle into a 1.50% to 1.75% range for the second half of 2026. Conversely, PGIM, the asset management arm of Prudential Financial, places a 40% probability on an “Overheating” base case for the U.S., projecting 2.3% GDP growth driven by robust corporate capital spending, fiscal expansion, and a wealth-effect consumption boom among high-income households.

The Corporate Earnings Powerhouse

If economic growth has moderated, corporate earnings remain the roaring engine of this bull market. First-quarter S&P 500 earnings results were exceptionally strong, showing an impressive 28% year-over-year blended growth rate.

This earnings strength has led several major banks to aggressively upgrade their equity market targets. Goldman Sachs Research raised its year-end 2026 S&P 500 price target to 8,000, projecting S&P 500 earnings-per-share (EPS) of $340 for 2026 (a massive 24% annual growth rate). Goldman’s strategists estimate that the direct beneficiaries of AI infrastructure spending will account for roughly half of this total earnings growth. Morgan Stanley Research similarly raised its S&P 500 year-end target to 8,000, pointing to strong positive operating leverage and pricing power. J.P. Morgan Global Research also upgraded its year-end target to 7,800 on an estimated EPS of $350 (+29% year over year).

Crucially, Clark Capital Management Group raised its year-end S&P 500 target to 8,100, citing six consecutive quarters of double-digit earnings growth. Chief Investment Officer Sean Clark points out that individual investor pessimism remains a contrarian positive, with a record $7.9 trillion currently sitting on the sidelines in money market funds.

Inflation, Interest Rates and the “Cash Trap”

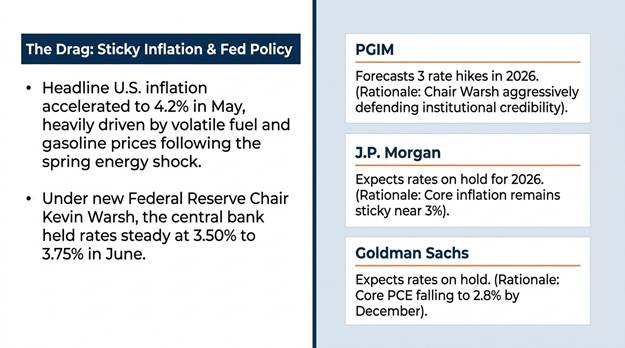

While growth and earnings are supportive, inflation remains sticky. Following the energy shock earlier this spring, headline U.S. inflation accelerated to 4.2% in May, heavily driven by volatile fuel and gasoline prices.

Under new Federal Reserve Chair Kevin Warsh, the central bank held rates steady at 3.50% to 3.75% in June. Major banks diverge on the Fed’s next move. PGIM expects Chair Warsh to aggressively defend institutional credibility, forecasting three rate hikes in 2026. Conversely, Morgan Stanley and J.P. Morgan expect the Fed to remain on hold for the remainder of 2026. J.P. Morgan’s strategists forecast that core inflation will remain sticky near 3%, while Goldman Sachs expects core PCE to fall to 2.8% by December.

For long-term investors, the message is clear: During periods of sustained inflation, excess cash may lose purchasing power over time. Since 2020, cumulative U.S. consumer prices have surged by 25%, while core fixed income has returned a mere 6%. Sitting on cash in an inflationary environment may result in a decline in real purchasing power if inflation exceeds the return earned on cash holdings.

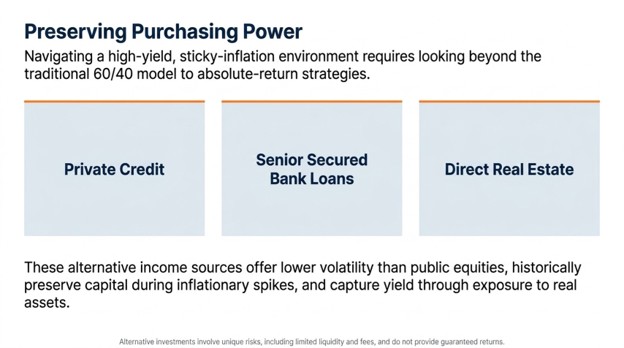

Diversification Beyond the Traditional

To navigate this high-yield, sticky-inflation environment, we believe investors must look beyond the traditional 60/40 stock-and-bond model. Non-traditional absolute-return strategies, including private credit, senior secured bank loans, and direct real estate, may help diversify portfolio risk in certain market environments. These alternative income sources offer lower volatility than public equities and historically preserve capital during inflationary spikes.

What You’re Missing

Are you tired of reading dry, 60-page financial PDFs just to figure out what to do with your portfolio? We’ve got you covered. We are proud to highlight the Halbert Wealth Management YouTube channel! We are bringing institutional-style investment insights straight to your screen in quick, clear, and engaging video and audio that avoid industry jargon.

Ready to learn more? Your action step for today:

Infographic Summary

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.