Given the recent controversy at the Bureau of Labor Statistics (BLS), it is a good time to examine the BLS and the general accuracy of its data.

What is the BLS?

BLS is the principal fact-finding agency of the U.S. government in labor economics. Its core functions revolve around providing objective economic data, evaluating its own performance, and adapting its methodologies to accurately reflect a changing economy.

BLS Forecast Types

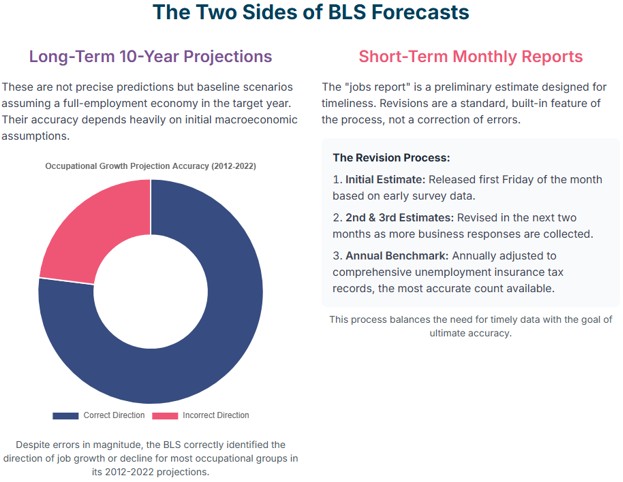

BLS forecasts come in two types. Long range 10-year projections and short-term monthly reports. Consider this infographic:

There is a lot of data in that graphic.

Long-Term Employment Projections: These are 10-year forecasts of employment across various industries and occupations. They serve as baseline scenarios, relying on fundamental assumptions about the U.S. economy. These projections offer a broad, long-term perspective on the economy's structure, rather than precise predictions. The process starts with labor force projections and utilizes models like the US Macro Model (MAUS) for overall economic analysis.

Short-Term Labor Market Data: The BLS also produces frequent short-term data, most notably the monthly Employment Situation report (known as the “jobs report”). The headline nonfarm payroll figure in this report is a preliminary estimate derived from the Current Employment Statistics (CES) survey.

Data Revision Process: It conducts two-step revisions for monthly estimates as more survey responses become available, and an annual benchmarking process to align CES survey data with more comprehensive state unemployment insurance tax records. This is a standard and transparent feature designed to balance timeliness with accuracy.

Case Study (2012–2022): The BLS projected an average growth rate for occupations of 10.8% over the decade, but the actual growth rate was 13.2%, an underestimation. This error primarily stemmed from inaccuracies in foundational macroeconomic assumptions, such as faster labor force growth and a lower actual unemployment rate in 2022 than projected. Despite magnitude errors, the projections demonstrated strong ability to identify underlying structural trends, correctly projecting growth or decline 77% of the time.

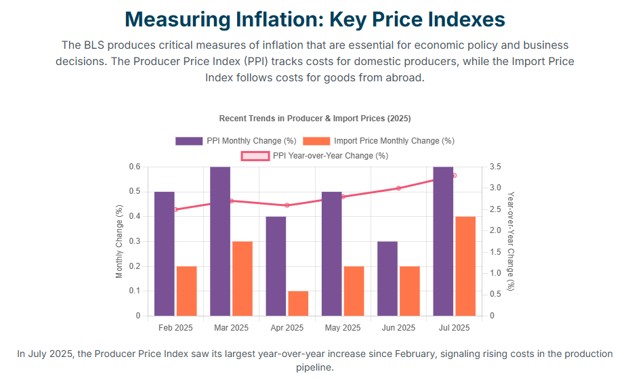

Measuring Inflation

Producer Price Index (PPI): The PPI gauges inflationary pressures within the production sector by tracking changes in the selling prices received by domestic producers for their output. For instance, in July 2025, the PPI for final demand rose by 3.3% over the preceding 12 months. This marked its largest year-over-year increase since February 2025, directly illustrating rising production costs.

U.S. Import Price Index: This index monitors increasing costs in the import pipeline by tracking the prices of goods imported into the U.S. In July 2025, the U.S. Import Price Index increased by 0.4% in that single month, primarily due to a 0.3% rise in nonfuel import prices. This provided further evidence of escalating import costs.

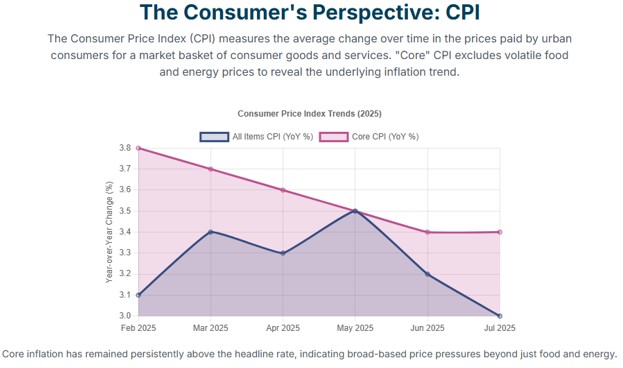

Consumer Price Index (CPI): The CPI measures pure price inflation for consumers, reflecting the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. The BLS demonstrates a commitment to adapting its methodologies to address structural changes in the economy. A recent example is the change implemented in July 2025 for calculating the CPI for wireless telephone services.

Overall, these price indexes serve as crucial objective data, enabling the BLS to measure and report on economic conditions, and providing foundational information for external research institutions to conduct policy-specific analyses, such as modeling the economic impact of tariffs.

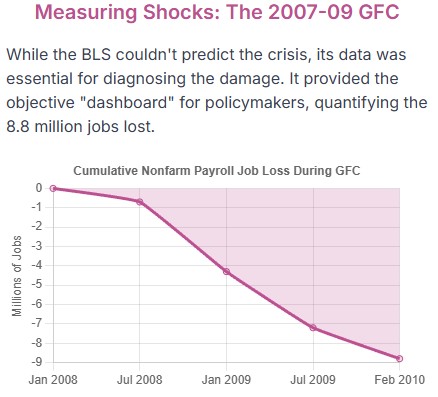

BLS Data and Systemic Shocks

The BLS exhibits limited predictive capacity and struggles to respond well to systemic shocks for several key reasons:

The BLS, like most forecasting institutions, struggles to predict economic turning points and structural shifts such as recessions or changes in labor productivity and oil prices. These unpredictable events are major contributors to forecasting errors across the economic field.

BLS long-term projections rely on fundamental assumptions about the U.S. economy, including labor force participation, energy prices, and fiscal policy. Systemic shocks can invalidate these assumptions, reducing the effectiveness of the forecast models. Errors in these initial macroeconomic and labor force assumptions inevitably impact final occupational projections; thus, misjudgments in overall economic pace or labor force growth can lead to significant errors in detailed forecasts.

The primary role of the BLS is that of a diagnostic tool, not a predictive one. The BLS's strength lies more in detailed post-event analysis and diagnostic capabilities than in predicting future shocks. Its mission is to measure and report on economic conditions, not to produce speculative forward-looking analyses on the potential impact of proposed legislation or executive actions. While it struggles to predict crises, it provides objective data crucial for understanding their impact and learning from them.

The BLS demonstrates a continuous commitment to improvement, with a long and well-documented history of refining its statistical techniques. This is evident in the multi-decade evolution of seasonal adjustment methods, transitioning from manual processes to the X-12 ARIMA (A modern process for data analysis.), each step informed by extensive testing and research.

The Bottom Line

BLS data is faulty but not rigged. Its initial reports always contain a form of large error. This is known and by design. That error is refined with a series of revisions. While its forecasting record is one of basic successes and its models outperform simple benchmarks, they struggle with structural breaks and turning points, similar to other institutions. Long-term projections serve as baseline scenarios and should not be assumed to be predictive.

The Bureau of AI Statistics

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.