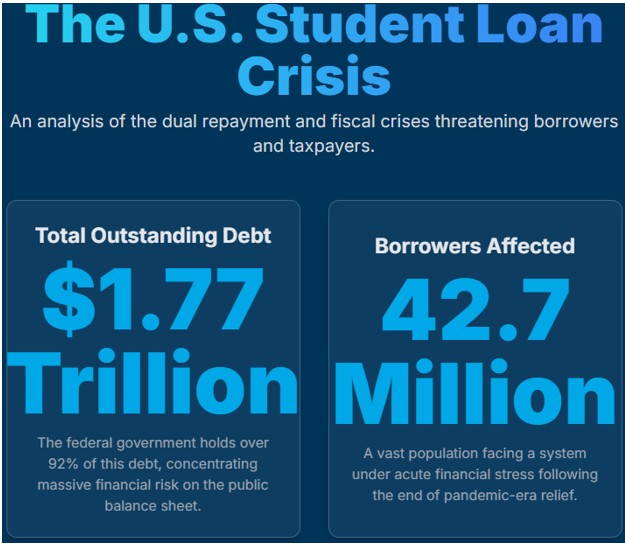

A severe crisis looms for the United States federal student loan system. The first is a severe repayment crisis. The second is one of fiscal unsustainability for the federal government. The current portfolio of student loan debt sits at $1.77T, an astoundingly large sum. The federal student loan system underwrites 92% of all student loans, equaling 42.7M borrowers.

A Crisis of Borrowers

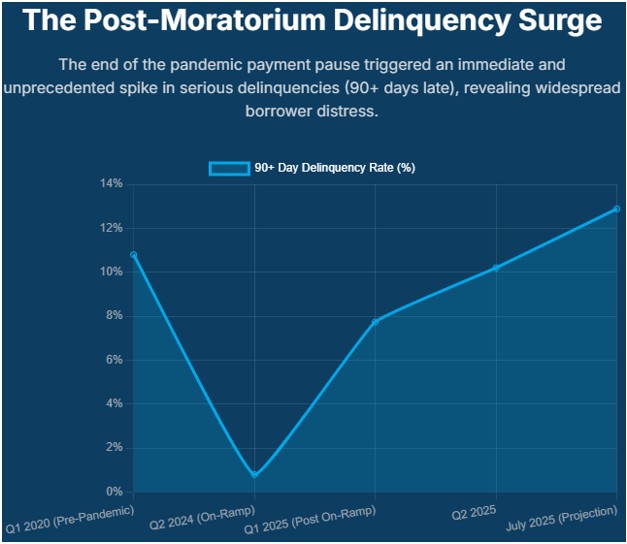

- Post-Moratorium Surge: The end of the pandemic payment pause has led to a dramatic spike in delinquencies. During the On-Ramp period, missed federal student loan payments started being reported to credit bureaus again after a five-year pause. In Q1 2025 the 90+ day delinquency rate jumped from less than 1% to 7.74% and climbed to 10.25% in Q2.

- The Velocity of Distress: The transition rate from current account to serious delinquency (90+ days late) skyrocketed from 0.80% in Q2 2024 to 12.88% in Q2 2025. This figure is alarming.

- Highest Ever Delinquency: As of April 2025, 31% of borrowers are seriously delinquent, nearly triple the pre-pandemic rate and the highest ever recorded. This strongly indicates a looming default crisis with as many as 1.8 million borrowers on track to default on their loans starting July 2025.

Profile Of The Distressed Borrower

Borrower distress is not uniform but it is heavily concentrated.

- Institution Type: Borrowers from for-profit colleges are more likely to struggle. In 2024, 35% of for-profit attendees were behind on payments, compared to 16% for public and 15% for private non-profit institutions. 851 (77%) of 1,110 institutions at risk of losing federal aid due to high nonpayment rates were for-profit.

- Educational Completion: Failure to complete a degree program is a significant risk factor. 30% of borrowers with some college or an associates degree were behind on payments versus only 11% for a bachelor’s degree and 8% for graduate degrees.

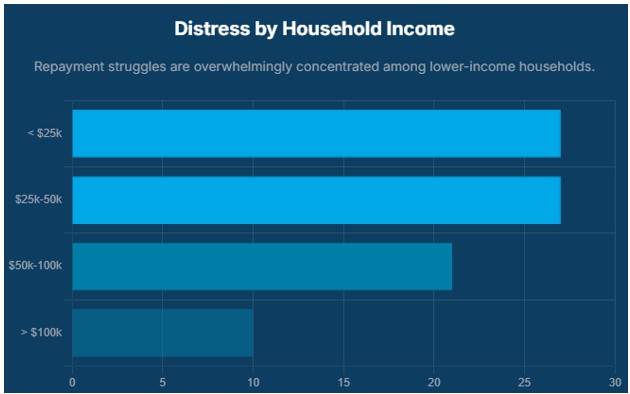

- Income Level: Repayment distress is a problem for lower income households. 27% of borrowers with an income below $50,000 are behind, compared to 10% for those earning $100,000 or more.

- Age: Contrary to popular belief – this surprised me – older borrowers show a high degree of distress. The highest rate of transition into serious delinquency in Q2 2025 was among those aged 50 and up. The average of a delinquent borrower has risen to 40.4 years.

Federal Fiscal Sustainability Crisis

- Federal Fiscal Sustainability Crisis: The second is a fiscal sustainability crisis for the federal government. Its student loan portfolio — now exceeding $1.64 trillion — has transformed from a projected source of income into a structural deficit driver. The portfolio is projected to cost taxpayers hundreds of billions of dollars over the next decade.

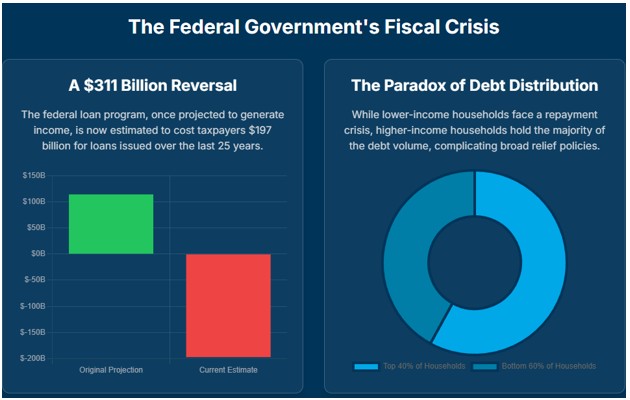

- Massive Cost Swing: The GAO found that Direct Loans issued from 1997-2021, originally estimated to generate $114 billion in income, are now projected to cost taxpayers $197 billion, a $311 billion negative swing.

- Future Costs: The CBO projects the federal student loan program will cost taxpayers $393 billion over the next decade (2024-2034), which is more than the entire projected spending on the Pell Grant program ($355 billion) over the same period.

A Trillion-Dollar Challenge

The total outstanding student loan debt in the U.S. has reached a staggering $1.77 trillion. The federal government holds the vast majority of this debt, approximately $1.64 trillion (92.4%), spread across 42.7 million borrowers. On average, each federal borrower carries a debt of around $38,375.

Federal student loan debt has experienced explosive growth, increasing at an average annual rate of 13.2% between 2007 and 2023.

A Policy Paradox: Debt Distribution and Repayment Distress

A significant policy paradox arises from the distribution of this debt. While repayment difficulties are more prevalent among lower-income borrowers, the largest volumes of debt are concentrated among those with higher incomes and advanced degrees.

- The wealthiest 40% of households, by income, account for 58% of all outstanding education debt.

- Households where individuals hold graduate degrees are responsible for 48% of the total student debt.

This distribution implies that broad-based policies, such as universal loan forgiveness, would disproportionately benefit those who are already financially well-off and are least likely to be experiencing repayment distress.

Consequences for Households and the Economy

Student loan debt significantly impacts borrowers' financial well-being and life choices, leading to:

- Credit Score Deterioration: In Q1 2025, over 2.2 million new delinquencies resulted in credit score drops exceeding 100 points, with 1 million experiencing declines of at least 150 points. This effectively bars borrowers from conventional credit markets.

- Reduced Economic Mobility: Households burdened with student debt possess an average net worth more than three times lower than the general population. A 1 percentage point increase in debt-to-income correlates with a 3.7 percentage point decrease in consumption.

- Delayed Life Milestones: Student debt delays major life events. 51% of renting borrowers have postponed homeownership, and it also contributes to delays in marriage and having children. Furthermore, it severely hinders retirement savings, with 84% of borrowers reporting a negative impact.

- Hindered Entrepreneurship: Individuals owing over $30,000 in student loans are 11% less likely to establish new businesses.

The Bottom Line

College costs are absurdly high which is a direct result of the ease of loan acquisition. Something must give. This situation is obviously unsustainable and is in the process of failing right now. A total collapse and crisis is likely on the horizon. The Big Beautiful Bill Act tightens lending requirements, but it does nothing to address the current portfolio. This $1.64 trillion toxic asset pool is only slightly smaller than the approximately $2 trillion toxic mortgage-backed asset pool from 2008-2009.

A taxpayer-funded bailout of the Federal Student Loan System is not some far off hypothetical event. It is on the verge of happening. With 42.7 million borrowers, there will be continued pressure on lawmakers to enact loan forgiveness programs. This is simply a bailout by another name. Unfortunately, large-scale defaults are coming and nothing will stop the collapse.

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.