Equity tokenization, converting traditional shares into digital tokens on a distributed ledger, promises to revolutionize global finance by creating more liquid, efficient, transparent, and accessible markets, unlocking trillions in value. However, widespread adoption faces three key hurdles: international regulatory agreement, digital ledger integration with existing infrastructure, and developing robust institutional platforms. This transformation is expected to be a phased, multi-year process.

Technology Powering On-Chain Equity

Tokenization revolutionizes ownership by converting shares into programmable, cryptographically secure digital assets on a shared, immutable ledger, replacing siloed databases.

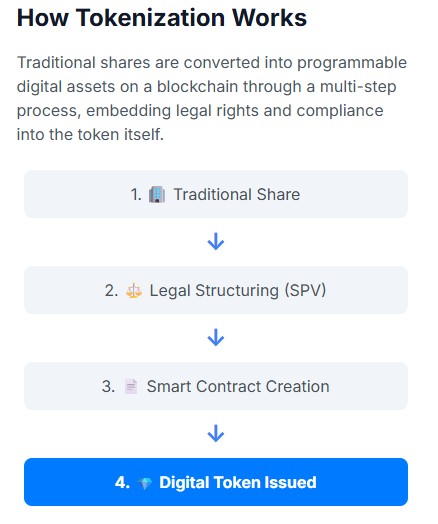

Equity Tokenization Process:

- Asset Identification & Legal Structuring: Often involves a Special Purpose Vehicle (SPV) to hold traditional shares, with tokenized SPV shares. Legal agreements define token rights (dividends, voting, transfer restrictions).

- Valuation and Due Diligence: Third-party valuation ensures fair market value.

- Smart Contract Development & Token Creation: Legal/financial terms encoded into smart contracts, which govern issuance, transfers, automated dividends, and on-chain voting.

- Token Issuance via Security Token Offering (STO): A regulated fundraising process requiring Know Your Customer and Anti-Money Laundering provisions.

Key Technologies:

- Distributed Ledger Technology (DLT): Typically, blockchain acts as a “single source of truth” for transactions, creating an immutable audit trail.

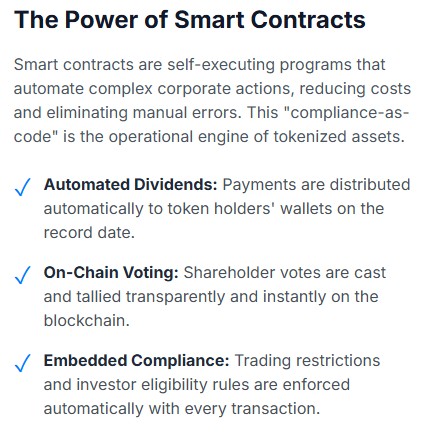

- Smart Contracts: Self-executing programs that automate corporate actions (e.g., automated dividend distribution, real-time vote tallying) and enforce compliance.

- Enforcing Compliance: “Compliance-as-code” embeds regulatory rules into tokens, preventing non-compliant actions by checking transactions against predefined criteria.

Compliance-Aware Token Standards:

- Integrated Identity Management: Requires verified on-chain identity.

- Programmable and Granular Compliance: Modular rules based on investor status or jurisdiction.

- Issuer Control and Asset Recoverability: Allows freezing/re-issuing stolen tokens, a vital safeguard.

Institutional-Grade Platforms: Major financial institutions are building end-to-end digital infrastructure for tokenized capital markets (HSBC Orion, Goldman Sachs DAP, Franklin Templeton Benji, J.P. Morgan Onyx).

Quantifying the Benefits of Tokenized Markets

Tokenization is set to revolutionize market dynamics by significantly boosting liquidity, efficiency, accessibility, and trust.

Enhanced Liquidity:

- Unlocking Illiquid Assets: Tokenization transforms illiquid assets such as private equity, real estate, and fine art into easily tradable digital tokens, potentially unlocking trillions of dollars in value. This expansion of access to alternative investments is projected to create a $400 billion annual new revenue opportunity, according to estimates by Bain & Co. and J.P. Morgan's Onyx.

- Fractional Ownership: The high divisibility of tokens allows high-value assets to be broken down into smaller, more affordable units, thereby democratizing access and broadening the investor base.

- 24/7 Global Markets: Blockchain networks facilitate continuous trading, leading to improved price discovery and greater flexibility in portfolio management.

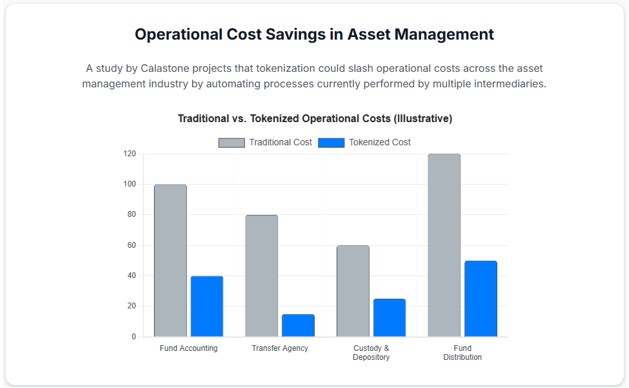

Operational Efficiency & Cost Reduction (Operational Alpha):

- Disintermediation and Automation: DLT and smart contracts automate or eliminate the roles of traditional intermediaries like registrars, transfer agents, and clearinghouses, resulting in streamlined processes.

- Quantifiable Cost Savings: Studies indicate substantial savings. Calastone forecasts “$135 billion in annual savings” for asset management, while Ghent University estimates “up to EUR 4.6 billion in Europe by 2030.” Furthermore, issuing securities via tokenization can be “35% to 65% cheaper than traditional securitization.”

- Near-Instant Settlement (T+0): Automatic settlement on DLT drastically reduces counterparty and settlement risk, freeing up billions of dollars in collateral and capital.

Democratizing Capital Formation:

- Accessing Global Investor Pools: Borderless blockchain networks enable STOs to reach a worldwide investor base, expanding funding sources.

- Streamlining Capital Raising: STOs are significantly more streamlined and flexible than traditional IPOs, offering benefits to small and medium sized enterprises.

A New Paradigm of Trust:

- Immutable and Transparent Audit Trails: Every transaction is permanently recorded on the blockchain, creating a perfect, unchangeable audit trail that enhances transparency and reduces fraud.

- Programmable and Cryptographically Secured Assets: Ownership is secured by private keys, and legal terms are embedded directly into the token's code, creating an inherently more secure and transparent asset.

Challenges and Risks

Despite the potential, tokenization faces significant regulatory, security, privacy, and integration challenges.

Regulatory Labyrinth: The primary obstacle is the absence of unified international regulation, resulting in a fragmented and complex legal landscape.

- United States (SEC): Applies the same business, same risks, same rules principle via the Howey Test (Determines what qualifies as a tradable security.). However, existing regulations for custody, transfer agents, and exchange registration present challenges. The SEC is exploring the idea of regulatory sandboxes (Controlled environments.) for tokenized securities.

- European Union (ESMA): Has been proactive with regulation, emphasizing technological neutrality, meaning tokenized securities fall under existing regulations. Although newer regulations are on the horizon.

- Asia (Hong Kong & Singapore): These regions are leading with pragmatic frameworks. Hong Kong's SFC employs a “see-through” approach, regulating based on the underlying asset. Singapore's MAS has a comprehensive Digital Token Service Provider (DTSP) regime with tiered licensing.

Digital Fortress (Cybersecurity, Theft, Custody):

- Primary Threat Vectors: Major risks include smart contract vulnerabilities, private key theft (leading to irreversible losses), and hacking of platforms or exchanges.

- Mitigation Strategies: These involve rigorous smart contract audits, institutional-grade custody solutions (e.g., multi-signature, cold storage, Hardware Security Modules), built-in asset controls allowing issuers to freeze or reissue stolen tokens (a crucial backstop), and specialized digital asset insurance.

Privacy Paradox: The inherent transparency of public blockchains conflicts with financial institutions' obligations to protect sensitive data.

- Solutions: This challenge can be addressed through permissioned DLTs, privacy-enhancing technologies like zero-knowledge proofs, and separating transaction data from sensitive Personally Identifiable Information (PII) via data tokenization and off-chain storage. In this approach, PII is securely stored off-chain, while on-chain tokens use non-sensitive references.

Integration Challenge:

- Technical Debt and Complexity: Integrating DLT with existing, decades-old monolithic legacy systems is a monumental task.

- Interoperability Problem: Fragmentation across various blockchains creates digital islands, impeding the formation of a single global liquidity pool. This requires universal standards for cross-chain communication.

- Institutional Inertia: Significant deterrents include high upfront costs, threats of disintermediation, and resistance to change from established players. Capital market infrastructure players have not yet shown a unified, concerted will to move markets onto DLT.

The Bottom Line

The tokenization of the securities markets is coming – slowly. For this to be accomplished by 2030 seems a stretch to me. International standards must first be decided upon. Certainly not an easy task. And is 24/7 trading of all securities even a good idea?

The benefits are vast but so are the hurdles required to make it a reality. This is, of course, one step closer to the tokenization of currency, something that the U.S. has so far resisted.

The Tokenization of AI

Spencer Wright is the Executive Vice President of Halbert Wealth Management, Inc. and the author of Forecasts & Trends. He has been with HWM for over 25 years.